SXCOAL

Published at

Weekly: Int'l thermal coal market sentiment cools, prices ease broadly

Global thermal coal market sentiment cooled somewhat over the week ended June 12, with prices easing modestly overall, though regional supply-demand divergence remained pronounced. The Asia-Pacific market held steady with a firmer undertone, supported by Chinese summer restocking and tightening Indonesian supply. Yet India remained largely absent from the seaborne thermal coal market amid robust domestic output and the approaching monsoon season. The European market turned quiet after completing summer restocking, with prices pulling back sharply as the geopolitical risk premium unwound.

On the supply side, spot availability of Indonesian coal stayed tight amid RKAB production quota constraints, while high-CV Australian coal partly filled the resulting supply gap. Russian coal held firm at Far East ports on the back of Asian demand, though north-western and southern ports continued to face pressure. South African coal traded in a narrow range, weighed down by India's continued absence and elevated freight costs.

Supply Side

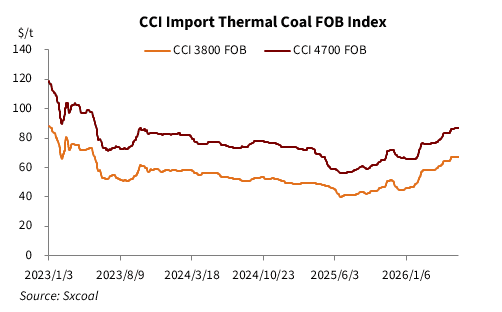

Indonesia Indonesia's thermal coal supply remained on the tighter side over the past week. Sources said some Indonesian miners have exhausted their production quotas and are awaiting the government's revision of the second-half RKAB. Pending clarity on new quotas, miners have generally adopted a conservative sales stance, avoiding overcommitting forward spot cargoes. Offers for July-loading Panamax 3,800 Kcal/kg NAR coal held above $70/t FOB.

As of June 12, the CCI Indonesian 3,800 Kcal/kg NAR coal index was assessed at $67/t FOB, unchanged week on week but up $2.3/t month on month. The CCI Import 4,700 Kcal/kg NAR index stood at $87/t FOB, also flat week on week and up $3.5/t month on month.

The transition period under Indonesia's newly established state entity, PT Danantara Sumberdaya Indonesia (DSI), tasked with tightening oversight of coal and other strategic resource exports, began on June 1 and is set to run through December 2026. However, the company's chief operating officer recently clarified that DSI's goal is to monitor transaction pricing and prevent transfer pricing and under-invoicing in order to boost state revenue, rather than to replace existing exporters or act as a resale intermediary, which added uncertainties on future export.

Even so, participants remained concerned about DSI's eventual operating model and its implications for traders' roles. Earlier uncertainty over the government's move to centralize commodity exports through a state-owned entity had already prompted some Asian buyers to pause negotiations on 2027 long-term contracts. Policy uncertainty, combined with limited spot availability among some miners, has kept Indonesia's spot market tight, with miners maintaining elevated price premiums.

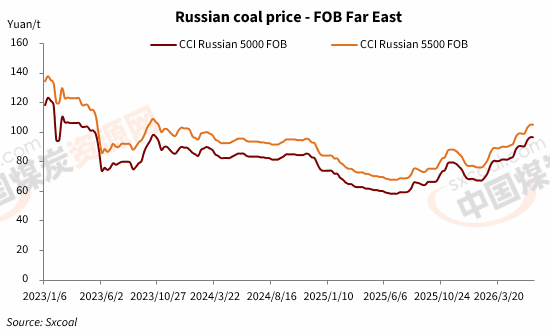

Russia Russian high-CV coal FOB prices at Far East ports rose $2-3/t over the past week, while gains at southern and north-western ports were comparatively smaller. The approach of summer, expectations of rising temperatures, and persistent Indonesian supply uncertainty continued to lend support to Asian thermal coal prices.

As of June 12, the CCI Russian 5,000 Kcal/kg NAR coal index at Far East ports was assessed at $96.5/t FOB, unchanged week on week but up $6/t month on month. Russian 5,500 Kcal/kg NAR coal was assessed at $105/t FOB, also flat week on week and up $6/t month on month.

Participants said inquiry interest from Northeast Asian buyers, including South Korea, remained steady at Far East ports, supporting shipments in that direction. Conditions at north-western and southern ports were comparatively weaker, mainly due to persistently subdued demand from Indian buyers, while the Turkish market reduced its purchases of Russian coal as the cement sector shifted toward more competitively priced petroleum coke, and lower freight rates on some routes failed to meaningfully stimulate demand.

Australia The Australian thermal coal market held relatively steady over the past week, with high-CV coal supported by stable demand from traditional Northeast Asian buyers, including Japan and South Korea, and prices edging higher. Sources said some South Korean buyers continued to seek South African coal for its price advantage, but limited South African availability left Australian coal holding a share of that demand.

As of June 12, Newcastle 5,500 Kcal/kg NAR coal was priced at $104.1/t, down $0.4/t week on week but up $5.3/t month on month, while the 6,000 Kcal/kg NAR grade continued to climb week on week, approaching $150/t.

Notably, a sharp drop in Capesize freight rates has made Newcastle 5,500 Kcal/kg NAR coal more price-competitive relative to the 6,000 Kcal/kg NAR grade, prompting some Japanese and South Korean buyers to shift toward purchasing 5,500 Kcal/kg NAR Australian coal to meet economic requirements.

A Singapore-based shipbroker noted that while demand from China has slowed, steady inquiries from Japan, South Korea and Southeast Asian countries including Vietnam provided underlying support for Australian coal prices. Separately, Taiwan's Taipower issued a tender on June 11 sourcing from Australia, Canada, Colombia, Indonesia and the United States, reflecting continued regional interest in Australian coal.

South Africa South African thermal coal prices stayed under pressure over the past week as traditional buyer India remained absent from the market. As of June 12, Richards Bay 5,500 Kcal/kg NAR coal was assessed at $94.49/t FOB, down $1.1/t week on week and $0.86/t month on month, while the 6,000 Kcal/kg NAR grade fell more than $3/t week on week to around $118/t.

Participants broadly attributed the weak seaborne demand to ample domestic Indian coal output, healthy Indian power plant inventories and elevated freight rates, with sponge iron sector demand particularly soft, directly weighing on South African high-CV coal sales. While inquiries from Japan and South Korea offered some support, they were not enough to offset broader market weakness stemming from the absence of Indian demand.

The bid-offer spread between buyers and sellers remained wide, with producers resisting price cuts amid rising operating costs, particularly a roughly 70% increase in diesel prices, while buyers held firm on lower purchase intentions, leaving spot transactions scarce.

Separately, a derailment involving a train operated by South Africa's state freight rail operator, Transnet, occurred near the Richards Bay terminal last week, disrupting several export rail lines. The market broadly viewed the incident's actual impact on coal exports as limited, as the prevailing weak demand environment had already diminished the price-supportive effect of supply chain bottlenecks.

Demand Side

China China's seaborne thermal coal import market showed mixed trends over the past week, with the prompt segment remaining under pressure even as sentiment toward the forward market stayed broadly bullish. On the demand side, domestic power plants continued tendering, with buyers leveraging ample near-term arrivals and lengthy port unloading queues to press for lower prices, pulling bid prices down.

As of June 12, the CCI Import 3,800 Kcal/kg NAR coal index at South China ports was assessed at $79.5/t CFR, down $0.5/t week on week. The 4,700 Kcal/kg NAR grade was assessed at $98/t CFR, down $0.5/t week on week, while the 5,500 Kcal/kg NAR grade held steady at $125/t CFR.

With temperatures rising across much of the country and power consumption increasing, coastal power plants maintained their restocking pace, with purchasing demand concentrated on low-CV Indonesian coal. However, participants noted that Chinese buyers were not particularly active, displaying a more cautious approach overall.

Some large power plants have already completed summer coal stockpiling, with inventories sufficient to cover roughly a month of consumption, leaving limited appetite for additional high-priced spot cargoes. Domestic coal output is expected to gradually recover as some mines complete safety inspections, easing the urgency for high-CV imported coal. In addition, congestion at southern Chinese ports and weather disruptions added uncertainty to near-term unloading and consumption.

India India's demand for imported thermal coal remained weak over the past week. Although the country has entered the summer peak power demand season, robust domestic coal output and comfortable power plant inventory levels left utilities with very limited need to purchase imported coal.

According to the Central Electricity Authority (CEA), Indian power plant coal stocks stood at 47.597 million tonnes as of June 14, down 0.62% week on week, with days of cover at 15.3 days, slightly below the prior week's 15.4 days. As of that date, 27 power plants were operating at critically low inventory levels, unchanged from the previous week.

Sources said most Indian buyers chose to stay on the sidelines, relying on more cost-competitive domestic coal supplies to meet demand. Elevated freight rates and relatively expensive import prices further dampened buying interest. With the monsoon season approaching, industrial power demand is expected to ease, reinforcing a cautious purchasing stance among end users.

Separately, local Indian traders said demand from the sponge iron sector remained similarly weak, with almost no active import inquiries observed. While power plant coal stocks have declined recently amid rising daily consumption, current inventory levels remain sufficient to meet near-term needs, making a large-scale return to the seaborne market unlikely in the short term.

Europe The European thermal coal market underwent a marked shift in sentiment over the past week. Early in the week, prices for ARA 6,000 Kcal/kg NAR coal remained supported by a geopolitical risk premium tied to tensions in the Middle East, but market risk appetite cooled sharply after news emerged on June 12 that the US and Iran could reach a diplomatic agreement and that the Middle East conflict might be nearing resolution, sending both gas and coal futures lower.

By late last week, ARA 6,000 Kcal/kg NAR coal CFR prices had plunged from above $160/t the prior week to around $132/t, a drop of more than $30/t.

Dutch TTF gas prices fluctuated higher over the past week. As of June 12, the ICE TTF benchmark Dutch gas futures contract for June 2026 delivery settled at 46.773 euros/MWh, down 3.55% from 48.496 euros/MWh a week earlier.

European end users have largely completed third-quarter restocking, leaving little urgency for spot purchases. Power producers and industrial users have mostly adopted a wait-and-see stance, awaiting clearer market signals. Local traders said the futures market decline could stimulate some spot demand in the coming weeks, but for now, end-user activity remains very limited and trading thin.

Source:

Other Article

Liputan 6

Published at

1,76 Juta Metrik Ton Batu Bara Disebar ke 4 PLTU Jaga Listrik di Jawa Tak Padam

Bisnis Indonesia

Published at

10 dari 190 Izin Tambang yang Dibekukan Sudah Bayar Jaminan Reklamasi

IDX Channel.com

Published at

10 Emiten Batu Bara Paling Cuan di 2024, Siapa Saja?

METRO

Published at

10 Negara Pengguna Bahan Bakar Fosil Terbesar di Dunia

CNBC Indonesia

Published at