SXCOAL

Published at

Weekly: Int'l thermal coal market extends gains on supply concerns, demand resilience

Global thermal coal markets extended their upward trajectory over the week ended June 5, driven by supply concerns and demand expectations from key consuming regions. While RKAB production quota constraints and the ongoing transition to Indonesia's single-window export regime continued to bring uncertainties to the near-term supply outlook. Russian coal held its ground through price competitiveness, and Australian prices firmed on robust demand from Japan and South Korea.

On the demand side, gas supply anxiety and restocking demand in Europe offered some support to South African and Colombian coal prices. Chinese import demand remained cautious, with buyers focused primarily on mid- and low-CV grades and showing limited tolerance for higher prices. Indian demand stayed persistently weak, with buyers continuing to lean on ample domestic supplies and increased renewable generation.

Supply Side

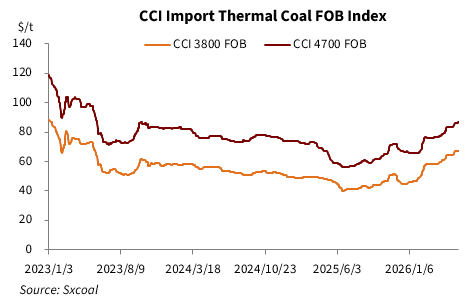

Indonesia Indonesian thermal coal market remained a focal point for global participants over the past week. Offers stayed firm, underpinned by ongoing uncertainty surrounding Indonesia's new centralized export reporting mechanism and relatively resilient international demand. Offers for June-delivering Panamax 3,800 Kcal/kg NAR coal were heard at $70-71/t FOB.

As of June 5, the CCI index for Indonesian 3,800 Kcal/kg NAR coal was assessed at $67/t FOB, down $0.4/t week on week but up $3.3/t month on month. The CCI Import 4,700 Kcal/kg NAR index rose to $87/t FOB, up $0.5/t week on week and $4.5/t month on month.

Market participants continued to assess the implications of the DSI transition on future contract arrangements, export procedures and cargo availability. Several Asian buyers reportedly deferred long-term negotiations, opting to wait for further policy clarity.

In the meantime, Indonesian miners maintained firm offers against a backdrop of tighter supply. Multiple coal grades were reported in short supply, partly due to ongoing rainfall and tight RKAB quotas. This, together with fuel shortages, raised operating costs and reduced miners' willingness to offer discounts.

While spot transactional activity slowed, lingering uncertainty over the supply outlook kept overall market sentiment firm.

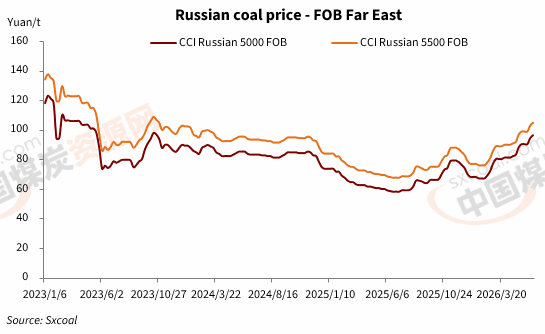

Russia Russian thermal coal market held broadly steady over the past week, with prices edging higher on the back of demand from Asian buyers seeking alternatives to Indonesian coal amid its export policy transition.

As of June 5, the CCI index for Russian 5,000 Kcal/kg NAR thermal coal at Far East ports was assessed at $96.5/t FOB, up $2/t week on week and $8/t month on month. Russian 5,500 Kcal/kg NAR coal was assessed at $105/t FOB, also up $2/t week on week and $8/t month on month.

With Indonesia's export outlook uncertain, some buyers actively sought Russian coal as an alternative. Russian high-CV grades tracked the broader market upward. Concerns over Colombian supply and stronger LNG prices in the EU also provided indirect support for Russian coal at north-western and southern ports. Besides, demand from the Turkish market remained stable.

Australia Australian thermal coal market posted a solid performance over the past week, with prices rising meaningfully. Market sentiment was supported by stable demand from Asia, in particular from Japan and South Korea, where LNG supply disruptions drove additional coal offtake.

As of June 5, Newcastle 5,500 Kcal/kg NAR thermal coal was assessed at $104.5/t FOB, up $1.5/t week on week and $7.7/t month on month. The 6,000 Kcal/kg NAR grade rose above $137/t FOB, gaining more than $10/t month on month.

Australian coal benefited from demand diversion as some buyers sought to reduce exposure to Indonesian supply uncertainty, particularly amid elevated mid- and high-CV Indonesian coal price premiums. Sustained Middle East tensions, rising European prices and limited high-CV availability from Indonesia collectively strengthened the competitive appeal of Australian grades in Asian markets.

South Africa South African thermal coal prices edged lower over the past week, weighed down by persistently weak demand from India. As of June 5, RBCT 5,500 Kcal/kg NAR coal was assessed at $95.6/t FOB, down $0.2/t week on week but up $1.1/t month on month. The 6,000 Kcal/kg NAR grade recovered slightly, edging up around $1/t week on week to hold near $121/t FOB.

Despite European demand offering support, direct purchasing interest from India remained weak, with buyers continuing to rely on domestic coal. Indian sponge iron producers, faced with low product prices and high import costs, were among the most prominent absentees from the market.

Transnet, South Africa's state rail operator, completed maintenance work on a second rail line and restored full rail service to RBCT, though the market expected the resumption to have a limited immediate impact on weekly export throughput volumes.

High operating costs kept seller offers firm, but limited buy-side interest left transaction activity broadly subdued.

Demand Side

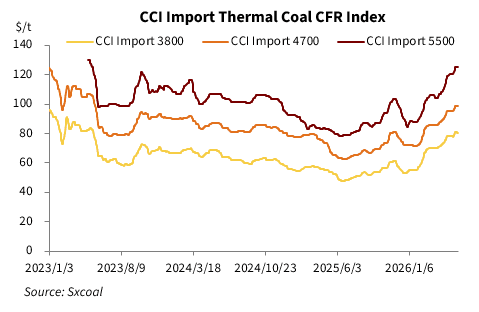

China Chinese thermal coal import markets held broadly stable over the past week, with buyers maintaining a cautious and selective approach. Although southern regions continued to record elevated power demand driven by the early onset of summer heat, import buyers showed limited tolerance for higher prices and focused their procurement on mid- and low-CV grades.

As of June 5, the CCI index for 3,800 Kcal/kg NAR coal was assessed at $80/t CFR South China, down $1/t week on week. The 4,700 Kcal/kg NAR grade held steady at $98.5/t CFR, unchanged week on week. The 5,500 Kcal/kg NAR grade was also flat at $125/t CFR.

China's domestic coal supply remained ample, and the impact of safety inspections on thermal coal remained manageable, as the stricter measures concentrated in the coking coal sector. No meaningful restocking of imported thermal coal was reported, while congestion at southern ports also dampened procurement activity. Some power plants still demanded low-CV Indonesian coal but were largely unwilling to take high-priced cargoes. With power plant inventories at comfortable levels, many buyers temporarily adopted a wait-and-see stance.

Market sentiment is expected to remain supported as the summer demand peak approaches and supply-side uncertainties persist, though short-term caution and price resistance among buyers are likely to remain the prevailing theme.

India Indian thermal coal demand remained persistently weak over the past week, as rising seaborne prices further dampened buying interest. Despite continued summer power demand, buyers largely remained on the sidelines, relying on domestic coal and renewable generation to meet load requirements.

According to the Central Electricity Authority (CEA), coal stocks at Indian power plants totaled 47.89 million tonnes as of June 7, down 2.58% week on week, with days of cover at 15.4 days, below the prior week's 15.9 days. As of that date, 27 power plants were operating at critical stock levels, up five from the previous week.

While power plant inventory levels have declined, they remained broadly sufficient to preclude emergency procurement. Indian buyers were largely absent from the market, purchasing only for immediate needs. Domestic coal continued to offer a more cost-competitive alternative to imports, and sponge iron producers also showed limited appetite for South African imported coal.

Europe European thermal coal markets rallied sharply over the past week, driven by gas supply concerns, geopolitical uncertainty and opportunistic restocking demand from utilities. By late in the week, ARA 6,000 Kcal/kg NAR thermal coal climbed above $165/t CFR, a gain of approximately $40/t week on week.

As of June 5, the ICE TTF benchmark Dutch gas futures contract for June 2026 delivery settled at 48.496 euros/MWh, up 5.4% from 46.001 euros/MWh a week earlier.

European utilities, many of which had already secured the bulk of their near-term coal requirements, continued to receive support from broader energy security concerns. The Cerrejon force majeure, though soon ended, would still impact high-CV coal supply, adding upward pressure to spot prices. Separately, the breakdown of US-Iran negotiations, resulting in strikes on Middle Eastern energy infrastructure, pushed oil and gas prices higher and reinforced the case for coal-fired generation.

ARA ports restocking and the forecast of a strong El Nino event provided additional price support in the EU market.

Source:

Other Article

Liputan 6

Published at

1,76 Juta Metrik Ton Batu Bara Disebar ke 4 PLTU Jaga Listrik di Jawa Tak Padam

Bisnis Indonesia

Published at

10 dari 190 Izin Tambang yang Dibekukan Sudah Bayar Jaminan Reklamasi

IDX Channel.com

Published at

10 Emiten Batu Bara Paling Cuan di 2024, Siapa Saja?

METRO

Published at

10 Negara Pengguna Bahan Bakar Fosil Terbesar di Dunia

CNBC Indonesia

Published at