SX Coal

Published at

Weekly: China's thermal coal prices rebound on pre-holiday restocking

China's domestic thermal coal market rebounded last week, thanks to pre-holiday replenishment and tightening supply caused by month-end production suspensions and early holiday leave at a few mines. The mine-mouth market also strengthened, with improved dispatches and eased inventory pressure prompting miners to lift offers.

Indonesian low-CV coal price rose at an accelrated rate on the back of tight supply, and Australian high-CV grade also gained on price rises in China.

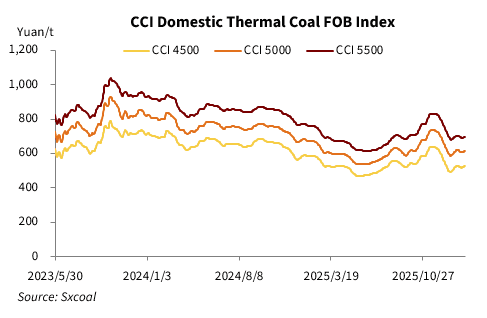

Sxcoal CCI Index

On January 30, the CCI index for 5,500 Kcal/kg NAR domestic spot coal stood at 696 yuan/t FOB northern China port with VAT, rising 5 yuan/t week on week, while the CCI index for 5,000 Kcal/kg NAR domestic coal was up 7 yuan/t from a week earlier to 614 yuan/t.

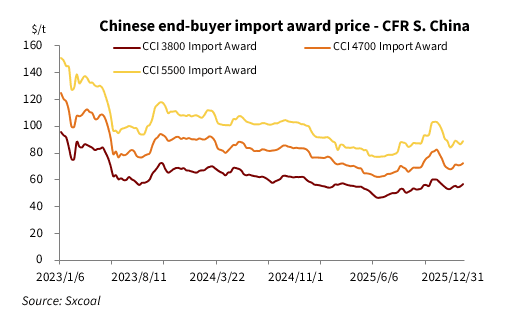

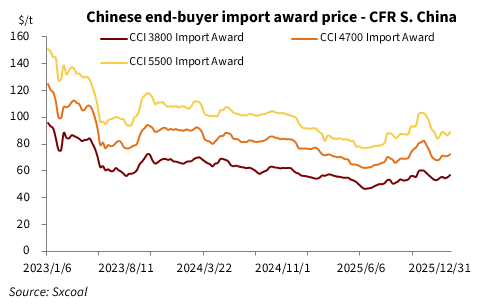

On the same day, the CCI 5500 Import index stood at $89/t, CFR southern China port, climbing $1.5/t compared with the previous week. The CCI 4700 Import index was up $1.3/t to $72.5/t, and the CCI 3800 Import index also gained by $1.8/t to $57/t.

Weekly Dynamic

Production areas saw prices edge higher last week, supported by tighter supply and a modest pickup of demand ahead of the Chinese New Year holidays.

A few miners suspended production towards the end of the month, after completing their monthly output targets. Several miners had already started their Chinese New Year holiday early, leading to marginally tightened supply.

With the festival approaching, a number of end users released restocking demand, helping smooth sales at some mines. Meanwhile, improved sentiment at the portside market and a leading miner's upward adjustment in third-party coal buy prices boosted mine-mouth sentiment.

The average capacity utilization of Sxcoal-surveyed mines in Shanxi, Shaanxi, and Inner Mongolia inched lower by 0.49 percentage point from the previous week to 89.8% during the week ended January 28. Their output also fell 0.54% on the week to 16.36 million tonnes. Improved sales reduced their coal inventory by 1.18% to 4.11 million tonnes.

More mines raised prices, while those cutting prices declined. Data showed that 21 out of the surveyed 160 thermal coal mines cut prices by 23.2 yuan/t averagely over January 22-28, compared with 50 mines lowering prices by 22 yuan/t a week earlier; 26 mines raised prices by 24.2 yuan/t, compared to 9 mines hiking prices by 17.8 yuan/t a week ago. The remaining 112 mines kept prices flat.

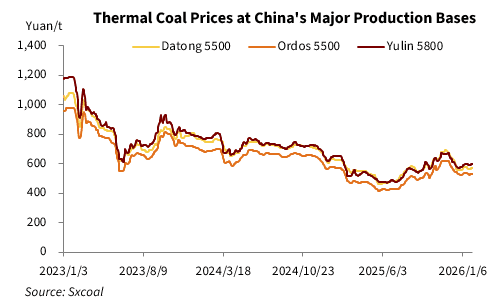

On January 30, Sxcoal assessed Yulin 5,800 Kcal/kg NAR thermal coal at 596 yuan/t, mine-mouth with VAT, rising 7 yuan/t from the preceding week; Ordos 5,500 Kcal/kg NAR coal gained 6 yuan/t to 532 yuan/t; and Shanxi Datong 5,500 Kcal/kg NAR coal was assessed at 568 yuan/t, climbing 4 yuan/t from the previous week.

Some participants noted that end-user demand remained moderate and insufficient to sustain a prolonged price uptrend. However, as year-end approaches, both coal mines and some end users are set to halt operations for the holiday, possibly leading to weak supply and demand and keeping prices range bound.

Portside market turned slightly stronger. Traders largely held prices firm and some slightly raised prices for low-sulfur and premium grades in the wake of low availability and rebounding inquiries ahead of the holiday.

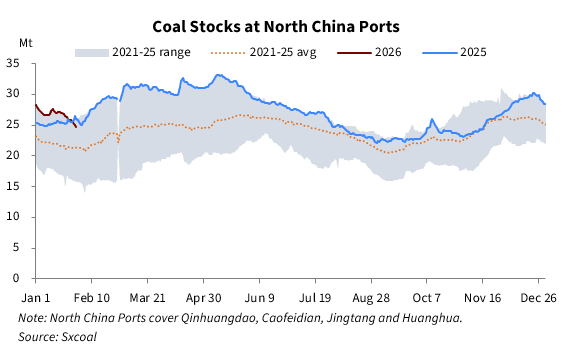

Coal stocks at Bohai-rim ports extended decline amid still low rail coal inflows. Coal deliveries through Daqin railway, a major transport artery connecting production areas to northern ports, rebounded by 2.1% week on week to 1.04 million tonnes during the week ended January 30. China Railway Hohhot Group, which supervises the rail networks in central and western Inner Mongolia, approved 16 trains to transport coal each day on average last week, down 1 from a week earlier.

Sxcoal's data showed the combined inventories at Qinhuangdao, Jingtang, Caofeidian, and Huanghua ports totaled 24.69 million tonnes on January 30, down 6.10% from the previous week and 13.29% month on month.

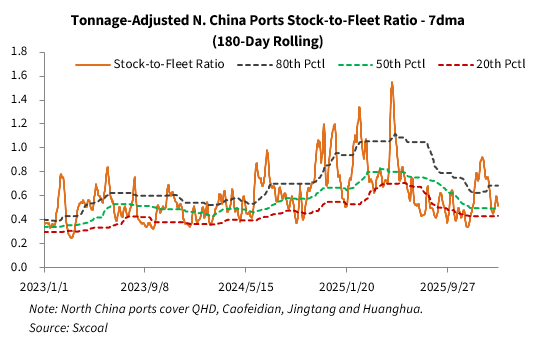

The tonnage-adjusted stock-to-fleet ratio, a major gauge for on-sight supply at northern ports, dipped marginally to 0.51 on January 30, staying slightly above the six-month rolling 50th percentile, according to Sxcoal's assessment, indicating a roughly balanced supply and demand pattern.

Some power plants and non-power end users slightly increased inquiries to build stocks ahead of the holiday, but their resistance to high prices resulted in a slow increase in transaction prices.

Data showed that coal consumption at inland power plants, which mainly rely on domestic resources, retreated by 1.8% week on week as of January 28, following a steep increase a week earlier. It was still 18.2% higher than the preceding month.

Some participants said recent mine price increases, persistent losses on port-bound supplies, and falling inventories have reduced the availability of tradable cargoes, providing support to portside prices.

However, some warned that demand from non-power sectors is expected to weaken as factories shut ahead of the Chinese New Year, limiting further upside and potentially returning the market to a stalemate.

Hydropower generation remained fluctuating. Sxcoal's data showed that water outflow through the Three Gorges dam, a key indicator of China's hydropower generation, reduced by 13.2% from a week ago to 7,980 cu.m/s on January 30. That climbed 6.7% from the preceding month yet fell 4.1% compared with the preceding year.

Import market Indonesian thermal coal prices slightly moved upward, backed by tight supply. Heavy rainfall disrupted production and delivery, forcing several miners to declare force majeure. Slow RKAB mining quota approvals and a sharp reduction for some mines that have received their quotas, coupled with continued constraints in South Sumatra due to coal transport bans on public roads, also affected supply.

Offers for Indonesian 3,800 Kcal/kg NAR coal on Panamax vessels were heard at $50-51/t FOB. Utility tender prices also gained as firm offers and rebounding seaborne freight rates pushed up delivered costs and prompted traders to lift their bidding prices.

On January 30, Sxcoal assessed the utility tender-winning prices for 3,800 Kcal/kg NAR coal at 445 yuan/t CFR South China with VAT, falling 12 yuan/t compared with 433 yuan/t in the preceding week.

Demand for high-CV Australian coal strengthened moderately, driven by improved sentiment in China's domestic market and expected pre-holiday replenishments from end users.

However, faster increases in imported coal further narrowed their price advantage. Sxcoal's calculation showed on January 30 that Indonesian 3,800 Kcal/kg NAR coal enjoyed a delivered-to-South China advantage of 8.17 yuan/t against domestic 4,500 Kcal/kg NAR coal on a CV-adjusted basis. That contracted by 9.18 yuan/t week on week.

On the same day, Australian 5,500 Kcal/kg NAR coal was assessed 25 yuan/t cheaper compared with the domestic equivalent on a landed basis, narrowing by 8.4 yuan/t week on week.

Forecast

China's domestic thermal coal prices are likely to stay firm this week, backed by declining production ahead of the holiday. Portside prices are also likely to be underpinned by pre-holiday restocking and tight supply of some premium grades. The seaborne import market is hopeful to inch up further as supply constraints have yet to be solved, though the upward space could be constrained by a lack of robust demand from end users.

Source:

Other Article

Liputan 6

Published at

1,76 Juta Metrik Ton Batu Bara Disebar ke 4 PLTU Jaga Listrik di Jawa Tak Padam

Bisnis Indonesia

Published at

10 dari 190 Izin Tambang yang Dibekukan Sudah Bayar Jaminan Reklamasi

IDX Channel.com

Published at

10 Emiten Batu Bara Paling Cuan di 2024, Siapa Saja?

METRO

Published at

10 Negara Pengguna Bahan Bakar Fosil Terbesar di Dunia

CNBC Indonesia

Published at