SXCOAL

Published at

Monthly: int'l thermal coal market diverges in Apr as geopolitical risks drive volatility

The international thermal coal market showed divergent and volatile trends in April, with prices fluctuating amid shifting geopolitical tensions and uneven regional supply-demand fundamentals.

Escalating conflict in the Middle East triggered sharp swings in global oil and gas prices during the start of April, pushing up high-CV thermal coal prices in Europe and Australia. However, energy product prices retreated quickly in mid-April after the U.S. and Iran reached a temporary ceasefire agreement, easing geopolitical risk premiums.

Toward the end of the month, renewed uncertainty surrounding the Strait of Hormuz once again fueled volatility, causing thermal coal prices to fluctuate accordingly.

At the same time, in China, power demand remained seasonally weak, with coal burns at utilities staying low. Combined with the significant price advantage of domestic coal, this reduced buying interest for imported cargoes. Indian buyers also largely stayed on the sidelines, relying on existing inventories to meet near-term demand.

On the supply side, tightening availability of low-CV Indonesian coal supported sellers' pricing sentiment and limited downside pressure.

Overall, sentiment in the international thermal coal market shifted rapidly from bullishness to caution during April, as geopolitical developments and market fundamentals continued to compete for influence.

Supply Side

Australia Australia's thermal coal market showed divergent trends in April. At the beginning of the month, escalating tensions in the Middle East pushed up global LNG and alternative fuel costs, driving Australian high-CV coal prices to a 17-month high.

However, prices retreated sharply in mid-April as geopolitical risk premiums eased. In contrast, Australian mid-CV coal prices remained relatively firm, supported by steady demand from Asia-Pacific buyers and continued enquiries from Chinese importers.

As of April 24, 5,500 Kcal/kg NAR thermal coal at Newcastle port stood at $92.49/t, up 7.09% or $6.12/t from the end of March, marking the highest level since early March 2024.

In addition to geopolitical factors, supply disruptions also lent support to prices. In early April, coal shipments along Queensland's West Moreton rail line was disrupted by a dispatcher strike, while scheduled rail maintenance between April 3 and 26 further tightened logistics capacity and delayed shipments.

Meanwhile, parts of the Hunter Valley rail network also experienced temporary closures for maintenance. Although spot buying interest for seaborne high-CV coal in Asia remained subdued, supply uncertainties were sufficient to keep prices relatively elevated.

In addition, traditional importers such as Japan and South Korea continued to secure high-CV cargoes under long-term contracts, while Southeast Asian buyers including Vietnam and the Philippines turned to Australian coal to supplement tightening Indonesian supply, helping underpin the market.

Indonesia Indonesia's Ministry of Energy and Mineral Resources (ESDM) adjusted up most of its benchmark coal reference prices or the HBAs (Harga Batubara Acuan) for H1 of April, and raised all of them for H2.

The HBA for 6,322 Kcal/kg GAR coal was set at $99.87/t in H1 and $103.43/t in H2. The HBA I, gauging 5,300 Kcal/kg GAR, was priced at $72.28/t in H1 and $77.71/t in H2, while the HBA II, measuring 4,100 Kcal/kg GAR, was set at $49.99/t in H1 and $52.84/t in H2. The HBA III, basis 3,400 Kcal/kg GAR, was set at $35.23/t for H1 and $38.3/t for H2, respectively.

Indonesia's thermal coal supply remained tight in April. Persistent rainfall in regions including South and Central Kalimantan, and El Nino effect disrupted mining operations and reduced spot cargo availability, strengthening miners' pricing sentiment.

Although Indonesia's energy ministry approved around 580 million tonnes of coal production quotas for 2026, approaching its 600 million tonne target, and allowed miners to apply for additional quotas later, producers prioritized fulfilling domestic market obligations (DMO). High-CV coal were mainly directed to domestic smelters and power plants.

On the demand side, enquiries from buyers in India, Bangladesh and Vietnam increased, providing support for Indonesian low- and mid-CV coal. By contrast, Chinese buyers continued to pressure prices lower, while relatively comfortable inventories and the price advantage of domestic Chinese coal constrained upside potential for Indonesian cargoes. The persistent gap between buyer bids and seller offers also limited spot trading activity.

In addition, plans by the Indonesian government to raise mining royalty rates and potentially introduce export taxes added uncertainty over future supply costs.

On April 28, the CCI index for Indonesian 3,800 Kcal/kg NAR coal stood at $62.5/t FOB, rising $4.3/t from the previous month; the CCI Import 4700 index stood at $81/t FOB, up $4.5/t month on month.

South Africa South African thermal coal prices came under pressure in April amid weak seaborne demand and intensifying competition in export markets.

As of April 24, South African 5,500 Kcal/kg NAR thermal coal prices stood at $89.85/t, down $5.96/t or 6.22% from the end of March.

Prices initially strengthened on firmer demand from Europe, but South African coal later lost competitiveness as European buyers increasingly turned to lower-priced alternatives from Colombia and the U.S. At the same time, Indian buyers slowed procurement due to elevated prices and volatile freight costs, further weighing on demand in key import markets.

Nevertheless, demand from alternative markets provided some support. Pakistan sharply increased imports of South African coal amid severe LNG shortages, while Sri Lanka began receiving South African cargoes following power generation disruptions linked to coal quality issues.

In addition, India's cement sector increasingly shifted toward South African high-CV coal as a substitute for petroleum coke, whose prices have risen sharply.

Overall, South African coal prices showed some resilience, though upsides remained limited due to sluggish demand and stronger competition.

Data from the country's customs showed its thermal coal (bituminous and sub-bituminous) exports reached 6.18million tonnes (Mt) in February 2026, up 7.7% year on year (YoY) but down 1.46% month on month (MoM). RBCT shipments totaled 6 Mt, a rise of 13.51% YoY but down 1.92% MoM.

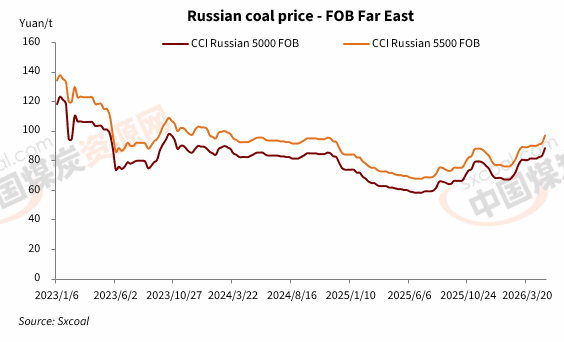

Russia Russian mid- to high-CV thermal coal prices continued to edge higher in April, although gains narrowed from the previous month.

As of April 24, Sxcoal assessed Russian 5,000 Kcal/kg NAR thermal coal at $83.5/t FOB Far East ports, up $2/t month on month; Russian 5,500 Kcal/kg NAR coal was assessed at $92/t, up $2/t from a month earlier.

Russian thermal coal remained active in April, particularly in Asia-bound trade. Supported by a clear price advantage, Russian high-CV coal attracted buying interest from China and India, while also increasingly serving as an alternative to high-priced Australian and U.S. cargoes in Asian markets, helping expand Russia's regional market share.

Indian cement producers showed particularly strong interest in Russian high-CV coal as international petroleum coke prices surged, leading to a notable increase in enquiries. At the same time, Turkey's cement sector continued purchasing Russian coal for cost reasons, with improving demand in Mediterranean markets also lending support to prices.

Kpler data showed Russia's seaborne coal exports totaled 9.86 Mt in March 2026, down 13.26% YoY and 13.18% MoM. Of this, thermal coal exports reached 6.91 Mt, falling 6.55% YoY and 2.33% MoM.

Demand Side

China China's imported thermal coal market remained subdued in April as seasonal weakness in electricity demand and ample inventories at utilities weighed on buying interest.

Spring is traditionally a low season for power consumption, with coal burns at utilities remaining relatively weak. By April 29, coal inventories at the six major coastal power plants reached 12.64 Mt, down 1.65% from the prior month. Daily coal burn averaged at 746,000 tonnes, a 2.23% fall MoM and a 1.97% YoY drop. The coal stockpiles enough for 17 days' consumption.

Most end users continued to rely on stockpiles and showed limited acceptance of high-priced imported coal, while actively seeking lower offers from suppliers.

At the same time, the growing price advantage of domestic coal further curbed import demand. Stable domestic coal prices and reliable long-term contract supply reduced the competitiveness of imported cargoes, with some imported grades even trading at a premium to comparable domestic coal.

Nevertheless, relatively high output in non-power sectors such as cement and chemicals continued to provide some support for selected coal grades.

Toward the end of April, some coastal utilities increased tenders for imported coal to secure summer supply, supported by maintenance on the Daqin Railway, rising temperatures in southern China and expectations that El Nino could lead to hotter weather after May.

Enquiries for Indonesian and Australian cargoes increased accordingly, although buyers remained highly price-sensitive and bid-offer gaps stayed wide, preventing large-scale restocking from materializing.

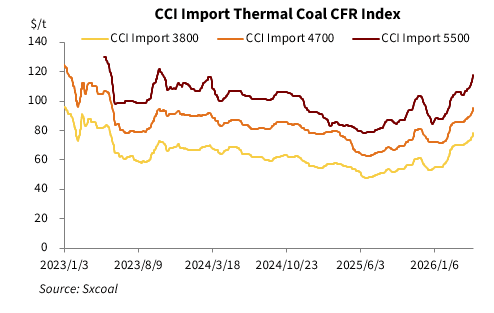

As of April 28, the 3,800 Kcal/kg NAR imported coal was $75.3/t CFR southern China, a $5.3/t increase from the end of March. The 4,700 Kcal/kg NAR coal was offered $92/t, up $6/t from the previous month. The 5,500 Kcal/kg NAR coal was $113/t, up $9/t.

As of the end of April, imported 3,800 Kcal/kg NAR coal was 34.7 yuan/t higher than the domestic equivalent grade, compared with 24.15 yuan/t at the end of March. The price gap between 4,700 Kcal/kg NAR cargoes and domestic equivalent expanded to 38.67 yuan/t from 25.24 yuan/t a month earlier.

Customs data showed China imported 26.64 million tonnes of thermal coal (excluding coking coal) in April, down 11.64% year on year but up 16.45% from February. Import value fell 14.03% to $1.68 billion, implying an average import price of $62.93/t, down $1.75/t from a year earlier.

Japan and S Korea In March, Japan's thermal coal imports (including other bituminous coal and other coal) reached 8.49 Mt, up 2.2% YoY but down 2.78% MoM. Of this, imports of other bituminous coal were 7.64 Mt, down 0.15% YoY and 5.63% MoM; imports of other coal stood at 0.85 Mt, up 29.58% YoY and 33.34% MoM.

South Korea imported 6.12 Mt of thermal coal in March, rising 46.41% YoY but falling 3.42% MoM. The country included 5.98 Mt of other bituminous coal, up 50.87% YoY but down 3.54% MoM, while imports of other coal totaled 140,400 tonnes, down 35.2% YoY but up 1.74% MoM.

India Indian buyers remained cautious in April, as comfortable utilities' inventories, ample domestic supply and elevated import costs continued to weigh on procurement interest.

High freight rates and fluctuations in the Indian rupee against the U.S. dollar further increased the cost of imported coal, prompting most end-users to rely on existing inventories and adopt a hand-to-mouth purchasing strategy.

Data from the Central Electricity Authority (CEA) showed that as of April 27, coal inventories at Indian power utilities stood at 54.42 Mt, down 7.02% MoM, enough for 17.6 days of usage, compared with 19 days at the end of March.

Strong domestic coal production and rising renewable power generation also reduced reliance on imported coal. Demand from India's sponge iron sector weakened significantly, as users were able to source lower-priced South African coal through domestic ports or switch directly to domestic coal.

By contrast, the cement sector increasingly turned to high-CV Russian and South African thermal coal as a substitute for petroleum coke, whose prices surged to multi-year highs. However, this replacement demand has yet to translate into large-scale spot transactions.

According to the Indian Ports Association (IPA), India's 12 major state-owned ports imported 18.89 Mt of coal in March 2026, up 14.93% YoY and 19.49% MoM. Of this, thermal coal imports were 12.91 Mt, up 13.22% YoY and 40.17% MoM.

India's power producers imported 2.98 million tonnes of thermal coal in the month, down 41.91% year on year and 8.73% from a month ago, showed data from the Central Electricity Authority (CEA). Among all the coal imported by power companies, 2.83 million tonnes were directly burned, while 152,900 tonnes were blended with domestic coal.

Source:

Other Article

Liputan 6

Published at

1,76 Juta Metrik Ton Batu Bara Disebar ke 4 PLTU Jaga Listrik di Jawa Tak Padam

Bisnis Indonesia

Published at

10 dari 190 Izin Tambang yang Dibekukan Sudah Bayar Jaminan Reklamasi

IDX Channel.com

Published at

10 Emiten Batu Bara Paling Cuan di 2024, Siapa Saja?

METRO

Published at

10 Negara Pengguna Bahan Bakar Fosil Terbesar di Dunia

CNBC Indonesia

Published at