SX Coal

Published at

Monthly: China's Jan coastal coal freight rates fluctuate at trough

China's coastal coal freight rates fluctuated at a trough in January, showing a month-on-month decline due to weaker cold wave impacts. Loose supply-demand dynamics for vessels have yet to improve, further weighing on the market.

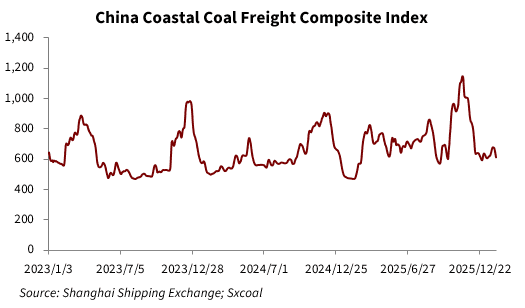

The China Coastal Coal Freight Composite index declined 3.13% compared to the end of December to 614.7 as of January 30, representing a year-on-year increase of 29.06%.

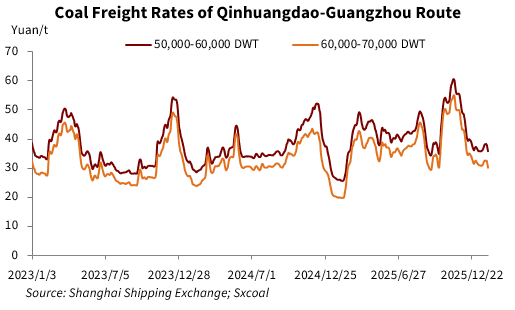

Freight rates on most routes from Qinhuangdao port showed downtrends in January. Notably, the 40,000-50,000 DWT vessels from Qinhuangdao to Zhangjiagang port dropped 5.8% on the month, while the 40,000-50,000 DWT Qinhuangdao to Shanghai vessels fell 5.3%.

On January 30, the freight rate for 60,000-70,000 DWT coal vessels on the Qinhuangdao-Guangzhou port route stood at 30 yuan/t, sliding 2.2 yuan/t or 6.8% compared to year-ago levels. The rate for the 15,000-20,000 DWT vessels on the Qinhuangdao-Ningbo port route rebounded 0.5 yuan/t or 1.3% on the month.

Entering January, spot coal prices at northern ports extended their rises, as de-stocking, firm cost support amid continued mine-mouth price hikes, and narrowing price advantage of imported coal encouraged sellers to lift offers.

However, elevated offers deterred purchases of some buyers, who remained cautious and reluctant to accept current prices. Amid relatively high inventories, they were largely inactive in purchasing. Market transactions continued to be at a standstill, with a persistent deadlock between buyers and sellers.

Meanwhile, the impact of strong winds and fog on coastal transportation was minimal and short-lived, failing to provide significant support to freight rates.

Against this backdrop, transactions in the coastal market remained lukewarm, maintaining relatively loose vessel supply and further weighing on freight rates for all routes.

Weather-led closures at northern ports, slightly improved demand, along with the bottom-level freight rates, encouraged vessel owners to firm up their offers in mid-January. As a result, rates on some routes saw modest increases, though overall levels remained at the bottom.

Large-scale cold waves boosted residential power loads, fueling restocking demand and consequently raising vessel demand in late January.

Additionally, southward-moving cold air and strong wind led to frequent port closures, severely impacting turnovers. The growing number of anchored vessels at ports tightened spot vessel availability, gradually improving market fundamentals and supporting coastal freight rates.

However, end-user shipments slowed at the end of the month, leading to an increase in idle vessels at northern ports. The loose supply-demand dynamics for vessels led to a retreat in freight rates.

The numbers of vessels at anchorage areas fluctuated sharply during January. In the month, the average anchored vessels were 95 at northern ports, up 27 from the previous month, while the average expected arrivals stood at 28, up 2 vessels on the month.

As of January 29, there were 98 anchored vessels, up 33 from late December and 45 vessels from the same period last year.

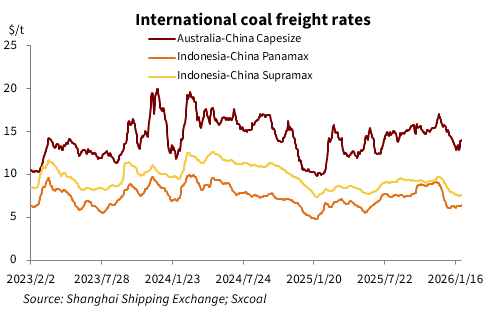

On the international front, the Baltic Dry Index (BDI) fluctuated significantly in January. While the Red Sea Crisis, China's transportation frenzy ahead of the Chinese New Year, and the seasonal delivery peak of agricultural products boosted demand, tight vessel supply and port congestion-led slow turnovers compressed available capacity. As of January 30, the BDI stood at 2,148 points, rising 13.71% from late December.

Coal demand followed a V-shaped trend, with freight rates rebounding in the second half of the month before staying low in the first half.

As of January 29, the freight rate for 85,000 DWT vessels from Hay Point, Australia, to Zhoushan, stayed at $11.63/t, up 3.65% or $0.41/t compared to late December. Similarly, for 70,000 DWT vessels from Samarinda, Indonesia, to Guangzhou, the freight rate stood at $6.33/t, increasing 4.11% or $0.25/t from the end of December.

As both sellers and buyers prepare for the holiday break ahead of the Spring Festival, weak supply and demand are expected to persist. Looking ahead, freight rates are expected to remain rangebound in February, with a low likelihood of weather-induced port closures.

Source:

Other Article

Liputan 6

Published at

1,76 Juta Metrik Ton Batu Bara Disebar ke 4 PLTU Jaga Listrik di Jawa Tak Padam

Bisnis Indonesia

Published at

10 dari 190 Izin Tambang yang Dibekukan Sudah Bayar Jaminan Reklamasi

IDX Channel.com

Published at

10 Emiten Batu Bara Paling Cuan di 2024, Siapa Saja?

METRO

Published at

10 Negara Pengguna Bahan Bakar Fosil Terbesar di Dunia

CNBC Indonesia

Published at