SX Coal

Published at

March 5, 2026 at 12:00 AM

China Feb domestic thermal coal robust; will it hold up in Mar?

China's thermal coal market defied its usual seasonal trend in February, with prices moving upward even as a long Spring Festival holiday dragged both supply and demand lower.

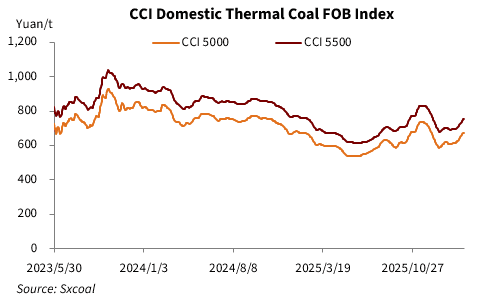

As of February 28, the CCI Index for 5,500 Kcal/kg NAR coal traded at Qinhuangdao port stood at 750 yuan/t, up 54 yuan/t from end-January and 69 yuan/t above the end of last year. The index for 5,000 Kcal/kg NAR coal was at 671 yuan/t, rising 57 yuan/t from the end of January.

With the weather improving, the winter peak season is ending. Prices are still edging upward, but the pace has clearly slowed, with low-CV coals stabilizing. What will support the market as it enters its typical off-season?

More plant burn but still well stocked

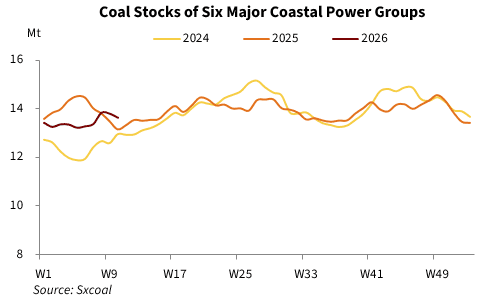

After the holiday, a gradual return to work and production lifted industrial electricity consumption, nudging up coal burn at power plants. As of March 3, daily coal consumption at the six major coastal power groups stood at 698,000 tonnes, up 19.42% from February 24, the first workday after the holiday, yet 15.23% below the same period last year, Sxcoal data showed.

This, together with inactive restocking interest due to seasonal weakness, led to inventory reductions. Stockpiles at those six power groups held 13.6 million tonnes, down 2% from the first post-holiday day. Still, the level was 3.23% above a year earlier.

Although coal consumption has increased moderately, large stockpiles will likely limit price gains during the upcoming off-season.

Supply resuming post-holiday

Coal mines in key producing regions are expected to fully restart operations after the Lantern Festival on March 3. Post-CNY holiday output has faced certain interruptions due to rain and snow in parts of the main production areas and a heightened emphasis on safety around the "Two Sessions".

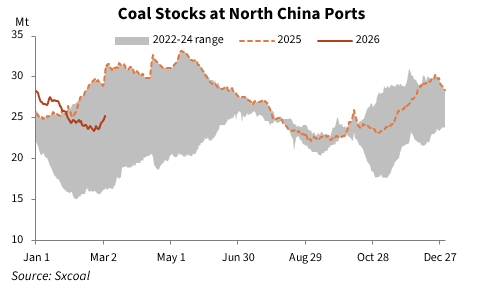

Coal inventories at northern ports have risen noticeably. Coal stocks at northern ports, including Qinhuangdao, Jingtang, Caofeidian, and Huanghua, reached 25.24 million tonnes by March 3, 6% higher than that on February 24, as per Sxcoal data. This figure remained in the mid-to-upper range of the past six years, even as it was 17.37% below last year's level.

Looking ahead, warmer temperatures and stronger renewable generation will weigh on coal demand. Northern ports are therefore likely to see inventory accumulation amid a loose supply-demand balance.

Imports remain a prop

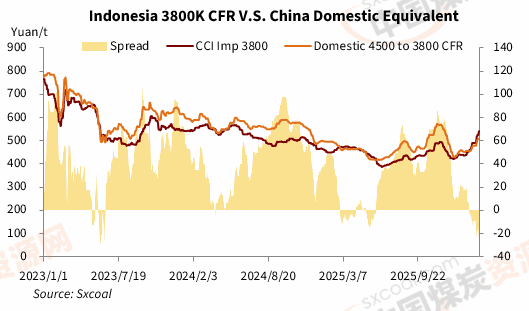

The main driver behind February's price rise came from imported coal. Against a backdrop of geopolitical conflict and the effects of Indonesia's RKAB policy, China's import procurement costs have continued to climb.

As of March 3, the CCI import index for Australian 5,500 Kcal/kg NAR coal arriving in South China was $103/t CFR, roughly 15 yuan/t higher than domestic same-CV coal delivered to the same southern port, compared with a 1.5 yuan/t deficit a week earlier.

Sxcoal calculations also showed that the imported Indonesian 3,800 Kcal/kg NAR coal prices were about 30 yuan/t more expensive than China's domestic 4,500 Kcal/kg NAR coal on a CV-adjusted and delivered-to-South China basis on the same day, with the spread widening by 13 yuan/t on the week.

With international coal prices still rising and expectations of tighter overseas supply lingering, Chinese end buyers may increasingly shift from imports towards domestic coal, which could provide some strength to the market.

However, the sustainability of this support remains uncertain. Over time, domestic utility procurement is likely to slow, and demand from non-power sectors such as chemicals and building materials looks sluggish. Indonesia's RKAB approvals are expected to be clarified soon.

March outlook

Uncertainty in international markets is likely to remain the main tailwind for China's domestic thermal coal prices for March. However, the fading of holiday disruptions should boost coal output and transport efficiency. Northern port inventories may begin to build, given adequate end-user stocks and expected seasonally lull consumption. With both bullish and bearish factors in play, thermal coal prices may swing in a narrow range.

Source:

Other Article

Liputan 6

Published at

1,76 Juta Metrik Ton Batu Bara Disebar ke 4 PLTU Jaga Listrik di Jawa Tak Padam

Bisnis Indonesia

Published at

10 dari 190 Izin Tambang yang Dibekukan Sudah Bayar Jaminan Reklamasi

IDX Channel.com

Published at

10 Emiten Batu Bara Paling Cuan di 2024, Siapa Saja?

METRO

Published at

10 Negara Pengguna Bahan Bakar Fosil Terbesar di Dunia

CNBC Indonesia

Published at