SX Coal

Tayang pada

Weekly: tight supply, firm Asian demand lift int'l thermal coal prices

International thermal coal prices remained firm over the past week, with tightening supply continuing to support prices, particularly in Indonesia, where supply constraints persisted due to slow approval of RKAB production quotas, DMO requirements and limited availability of high-CV coal. Seaborne high-CV coal cargoes also remained scarce, keeping prices elevated despite a lack of significant demand-side improvement.

On the demand side, China and some Southeast Asian countries maintained relatively active procurement of low-CV coal amid summer restocking demand, while Indian buyers largely stayed on the sidelines as ample domestic inventories continued to weigh on import appetite.

In Europe, coal prices also strengthened, driven by surging natural gas prices and geopolitical risks, although spot buying activity remained subdued.

Supply Side

Indonesia Indonesia's thermal coal market held firm last week as tight supply continued to support prices, particularly for forward-loading cargoes, while prompt shipments faced some selling pressure. Offers of Panamax Indonesian 3,800 Kcal/kg NAR coal stood at around $68/t FOB.

On May 15, the CCI index for Indonesian 3,800 Kcal/kg NAR coal stood at $64.7/t FOB, unchanged from the week-ago level and rising $4.9/t from the previous month; the CCI Import 4,700 index stood at $83.5/t FOB, flat week on week and up $5.7/t month on month.

Slow RKAB approval progress and limited approved output volumes continued to restrict spot availability. Several traders noted that high-CV coal was particularly scarce, with some miners prioritizing remaining production for Indonesia's state utility PLN and domestic smelters.

Rising diesel costs and ongoing logistics challenges also increased miners' production costs, exacerbating supply tightness. Meanwhile, Indonesian miners remained hopeful that RKAB production quotas could be raised in the future. However, until any adjustments are formally approved, supply conditions are unlikely to improve significantly in the near term.

Under the current tight supply environment, sellers continued to dominate the market and maintained firm pricing sentiment.

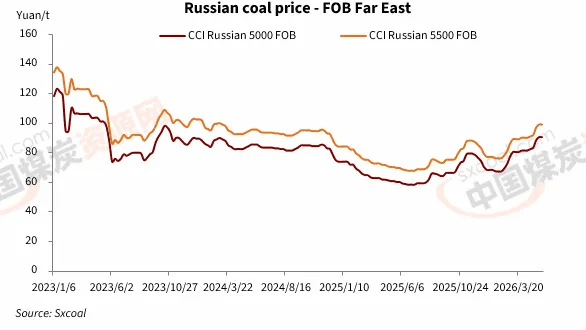

Russia Russia's thermal coal market remained active over the past week, supported by elevated Australian high-CV coal prices and tightening Indonesian supply, which improved the competitiveness of Russian coal in Asia-Pacific markets.

On May 15, Sxcoal assessed Russian 5,000 Kcal/kg NAR thermal coal at $90.5/t FOB Far East ports, unchanged on the week and up $9/t month on month; Russian 5,500 Kcal/kg NAR coal was assessed at $99/t, also unchanged from the week-before level and rising $9/t from a month earlier.

In Northeast Asia, buying interest from Japan and South Korea increased, with some sellers actively redirecting cargoes to the Korean market, where profit margins were viewed as more attractive than in China.

Market participants also noted that fluctuations in the Russian ruble continued to provide underlying support for U.S. dollar-denominated FOB prices.

Separately, market sources said Russian producers may prioritize fulfilling contract shipments in June rather than releasing additional spot cargoes, suggesting spot supply could remain tight in the near term.

Australia Australia's thermal coal prices at Port of Newcastle trended lower last week. As of May 15, 5,500 Kcal/kg NAR thermal coal at Newcastle port was at $98.69/t FOB, down $0.15/t from the week before but up $11.45/t from a month earlier. Prices of 6,000 Kcal/kg NAR coal dipped week on week to below $132/t.

Although demand in Northeast Asia, particularly from Japan and South Korea, remained relatively firm, sustained increases in prices and elevated freight rates prompted buyers to shift toward more cost-competitive alternatives.

Market sources said the landed cost of Newcastle 5,500 Kcal/kg NAR coal rose above that of comparable domestic Chinese coal, reducing the appeal of imports.

The widening gap between bids and offers slowed trading activity. While concerns persisted over potential weather disruptions and operational issues at mines on the supply side, high prices are increasingly weighing on demand in the short term, leaving Australian coal prices under pressure for a potential near-term correction.

South Africa Last week, South African mid- to high-CV thermal coal prices edged higher. As of May 15, 5,500 Kcal/kg NAR coal at Richards Bay Coal Terminal (RBCT) rose $1.27/t week on week to $96.62/t FOB, up $5.08/t month on month. The 6,000 Kcal/kg NAR materials climbed over $3/t to nearly $118/t.

Market sentiment at RBCT improved over the past week, largely supported by stronger demand from markets outside India. Asian buyers from Vietnam, Pakistan and South Korea showed increased interest in South African mid- and high-CV coal, partially offsetting persistently weak demand from India.

South African suppliers remained reluctant to lower offers, supported by bullish sentiment across global energy markets and elevated freight rates. However, cautious buying interest from India continued to cap the upside potential for South African coal prices.

Demand Side

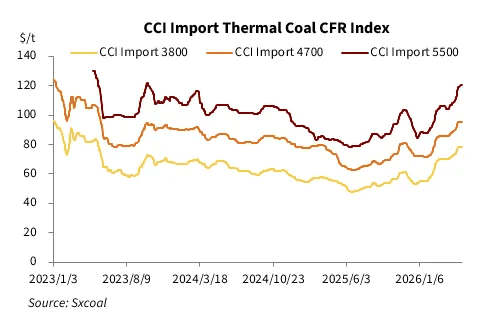

China As China approaches the power demand peak, domestic utilities continued to maintain steady, need-based restocking, keeping demand for low-CV Indonesian coal stable.

However, with the domestic thermal coal market largely steady and import costs rising, the price gap between imported and domestic coal widened again toward the end of last week, dampening market sentiment and prompting a more cautious, wait-and-see approach.

On May 15, Sxcoal assessed 3,800 Kcal/kg NAR coal at $78.5/t CFR South China, up $6.5/t from a week ago; the 4,700 Kcal/kg NAR coal was assessed at $95.5/t, up $0.5/t; and the 5,500 Kcal/kg NAR coal was assessed at $120.5/t, increasing $1.5/t from a week earlier.

By late last week, the price gap between imported 3,800 Kcal/kg NAR coal and equivalent domestic coal had expanded to an inversion of $9.15/t.

Ahead of the summer peak, utilities maintained essential restocking, particularly for Indonesian low-CV coal. Inventories at some southern power plants remained seasonally low, providing continued support for imports.

However, rising international coal prices and freight rates pushed up costs, leading to softer buying interest and more cautious procurement.

Following the completion of maintenance on Daqin railway, coal shipments recovered and portside inventories gradually increased, weakening the competitiveness of imported coal. At the same time, a stronger yuan partially improved import margins, offering some support to forward buying sentiment.

India India's thermal coal market remained subdued last week, as buyers continued to rely heavily on domestic supply despite tightening conditions across Asia and a decline in domestic coal output in April.

With inventories remaining relatively comfortable, procurement urgency stayed low and import demand remained weak.

By May 17, Indian power plants' coal inventories fell 2.55% from a week ago to 52.31 million tonnes, showed data from the Central Electricity Authority, which was available for 16.9 days of consumption. As of late last week, 23 plants operated at critical stock levels, up three plants from a week earlier.

Market participants said high international coal prices continued to face strong resistance from Indian buyers, with domestic coal substitution becoming increasingly prevalent, particularly in industries such as sponge iron.

Even coastal power and cement producers that typically rely on imported coal have been reassessing the feasibility of switching fuel sources. Overall, buyers remained on the sidelines, awaiting a price correction, leaving spot activity muted.

Europe European thermal coal markets were largely driven by energy security concerns and volatility in the gas market over the past week. By late last week, 6,000 Kcal/kg NAR thermal coal at the ARA ports extended the previous week's gains, rising above $107/t, up nearly $2/t week on week.

Escalating geopolitical tensions in the Middle East heightened concerns over global energy supply, pushing TTF natural gas prices to a more than one-month high. As of May 15, the gas futures contract for June 2026 delivery at the European benchmark TTF hub was closed at 50.167 euros/MWh, up 13.65% from 44.143 euros/MWh a week ago.

Rising gas prices improved coal's relative cost competitiveness in Europe's power sector, supporting gains in API2 coal futures and spot prices.

However, demand remained lackluster. Some European power plants underwent seasonal maintenance, while most utilities reported inventory levels sufficient to cover generation needs through the third quarter. Increasing renewable output also continued to cap near-term demand for coal-fired generation.

Sumber:

Artikel Lainnya

Liputan 6

Tayang pada

1,76 Juta Metrik Ton Batu Bara Disebar ke 4 PLTU Jaga Listrik di Jawa Tak Padam

Bisnis Indonesia

Tayang pada

10 dari 190 Izin Tambang yang Dibekukan Sudah Bayar Jaminan Reklamasi

IDX Channel.com

Tayang pada

10 Emiten Batu Bara Paling Cuan di 2024, Siapa Saja?

METRO

Tayang pada

10 Negara Pengguna Bahan Bakar Fosil Terbesar di Dunia

CNBC Indonesia

Tayang pada