SXCOAL

Tayang pada

Weekly: Int'l thermal coal market stays weak, prices under pressure

International thermal coal markets remained under pressure over the past week, with prices broadly declining as the U.S.-Iran memorandum of understanding eased Middle East tensions, reducing risk premiums in global energy markets and dragging down European gas and coal prices.

Chinese buyers stayed on the sidelines amid persistent rainfall in the south and high stockpiles at power plants, while Indian buyers also kept procurement low due to ample domestic supply, the approaching monsoon season and weak demand from the sponge iron sector.

On the supply side, Australian high-CV coal prices saw a notable correction as Chinese buying interest cooled. Indonesian low-CV coal prices softened alongside, though supply-side uncertainties from the RKAB quotas and DMO obligations provided a floor. South African coal prices came under pressure as Indian buyers shifted to domestic coal.

Indonesia

Supply-side uncertainties remained a key market variable over the past week, but their price-supportive effect is facing headwinds from weak demand. Tight availability of Indonesian coal in the seaborne market persisted due to slower RKAB production quota approvals and a potential rise in DMO allocation. However, FOB offers continued to weaken amid bearish buyer sentiment. Indonesian 3,800 Kcal/kg Panamax cargo was heard offered at $68/t FOB.

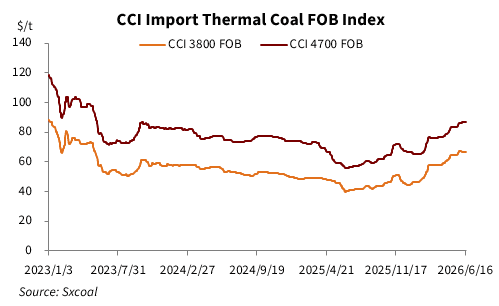

As of June 18, the CCI index for Indonesian 3,800 Kcal/kg NAR coal was assessed at $66.5/t FOB, down $0.5/t from a week earlier but up $1.8/t from a month ago. The CCI index for Indonesian 4,700 Kcal/kg NAR coal stood at $87/t FOB, flat week on week but up $3.5/t from a month earlier.

Market sources said the government may revise already-approved 2026 RKAB production plans to divert more supply to state-owned utility PLN. However, miners widely noted that even a 10 Mt production quota increase would not be approved until late July or August, with risks of further delays, giving miners an incentive to keep prices stable in the near term to optimize returns from limited output.

Meanwhile, the Indonesian government is seeking solutions to fill an annual coal supply gap of around 20 Mt for PLN. Energy Minister Bahlil Lahadalia said the government is carefully balancing the need to secure coal supply for domestic power plants with the survival of mining companies, as rising production costs for mid-CV coal and the DMO price cap of $70/t are squeezing miner margins.

Russia Russian thermal coal prices came under pressure over the past week, driven by easing global geopolitical tensions and cooling demand from key importers. At Far East ports, high-CV coal prices fell notably, with 6,000 Kcal/kg FOB offers down around $5-7/t week on week, while 5,500 Kcal/kg coal declined $1.5-2.5/t.

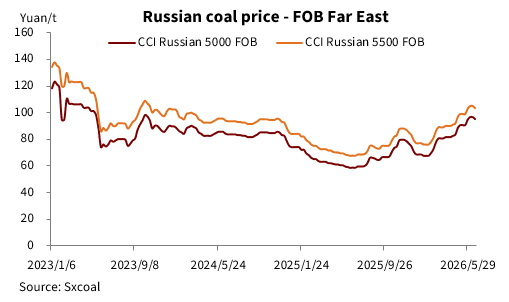

As of June 18, the CCI Russian 5,000 Kcal/kg NAR coal index at Far East ports was assessed at $95/t FOB, down $1.5/t from a week earlier but up $4.5/t from a month ago. Russian 5,500 Kcal/kg NAR coal was assessed at $103.5/t FOB, down $1.5/t week on week but up $4.5/t from a month earlier.

Despite the price decline, trading activity remained thin as major buyers China and South Korea showed little interest due to ample inventories and holiday factors. However, some market participants noted that Russian coal's competitiveness in Asia could improve in the coming months as summer peak power demand approaches and shipping costs decline, potentially supporting future shipments.

Australia Australian high-CV coal prices came under pressure over the past week as weak demand from major Asian importers kept buyers cautious. As of June 19, the price of 5,500 Kcal/kg NAR coal at Newcastle port fell below $100/t to $98.51/t FOB, down $5.61/t from a week earlier and $0.18/t from a month ago. The 6,000 Kcal/kg coal price dropped over $10/t from a week earlier to below $140/t.

The sharp price correction partly reflected cooling Chinese demand, as importers showed less interest in forward cargoes due to high stockpiles at domestic power plants and port congestion. The broader decline in energy prices amid easing geopolitical tensions also weighed on the Australian coal market.

However, fundamental factors — including ongoing mine safety inspections in China, lingering supply uncertainties in Indonesia, and the approaching peak summer power demand in North Asia — are expected to limit further downside.

South Africa South African thermal coal market remained weak. As of June 19, the FOB price of 5,500 Kcal/kg NAR coal at Richards Bay was assessed at $89.95/t, down $4.54/t from a week earlier and $6.67/t from a month ago. The 6,000 Kcal/kg FOB price fell nearly $10/t week on week to around $108/t.

On the demand side, Indian sponge iron producers showed very low interest in imported coal, prioritizing cheaper domestic coal as domestic finished steel prices weakened and sponge iron and pellet prices declined. The approaching monsoon season in India further reduced the urgency of imports.

Although state-owned freight operator Transnet suspended coal train operations due to a derailment, the incident had little impact on prices as Richards Bay Coal Terminal inventories remained above 4 Mt and buyer demand was weak. Market participants generally expect further downside for South African coal prices before the full onset of the Indian monsoon.

Demand Side

China Chinese thermal coal import demand remained subdued over the past week, weighing on Asia-Pacific prices. While expectations of an El Nino-driven heatwave and higher summer power demand persisted, high stockpiles at power plants and ports curbed immediate buying interest.

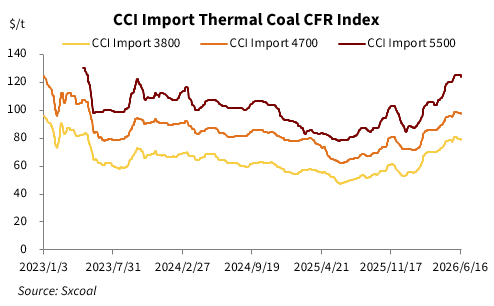

As of June 18, CCI Import 3,800 Kcal/kg NAR coal index at South China ports was assessed at $78.5/t CFR, down $1/t from a week earlier. The 4,700 Kcal/kg NAR grade was assessed at $97.5/t CFR, down $0.5/t week on week. The CCI Import 5,500 Kcal/kg NAR coal was assessed at $123.5/t CFR, down $1.5/t from a week earlier.

As of June 21, coal inventories at six major coastal power groups rose 1.9% week on week to 14.16 Mt, while port stockpiles also remained high. Persistent rainfall in the south suppressed power consumption growth, reducing the urgency for power plants to restock. Most buyers opted to delay purchases, waiting for clearer market signals.

Some large power plants continued to inquire for Indonesian low-CV coal in preparation for potential El Nino weather, but most coastal plants have shifted their focus to forward cargoes for late July and August loading. The Dragon Boat Festival holiday also saw some Chinese buyers step back, with most power plants and traders adopting a wait-and-see approach, only making limited inquiries for low-CV Indonesian coal, further dampening weekly market activity.

India Abundant domestic coal supply, weak pre-monsoon restocking demand and the low cost-competitiveness of imported coal continued to suppress Indian buyers' import demand over the past week.

Rising domestic coal output and improved logistics have made domestic coal easily accessible to end users at a clear price advantage. Meanwhile, the southwest monsoon has arrived and is advancing, reducing power demand and slowing some industrial activity, further lowering procurement urgency.

Indian power plant inventories remained at safe levels. Data from the Central Electricity Authority showed that as of June 21, coal stocks at Indian power plants stood at 46.125 Mt, down 3.09% from a week earlier, with an average of 14.8 days of stock, down from 15.3 days a week earlier. Thirty-one power plants were in critical low-stock status, up four from a week earlier.

Buyers remained cautious on imported coal, generally expecting further price declines and adopting a wait-and-see strategy. Only a few companies with urgent restocking needs made tentative inquiries, but bids were well below seller expectations and focused mainly on Indonesian mid- to low-CV grades. Sponge iron producers, hit by falling domestic finished steel prices and squeezed margins, have nearly halted inquiries for South African coal.

Europe The European thermal coal market cooled over the past week, in stark contrast to the active stockpiling seen in previous weeks, as geopolitical risk premiums faded and the seasonal peak procurement period ended. European power utilities largely withdrew from the spot market, with buying activity nearly grinding to a halt.

By late last week, the CIF price of 6,000 Kcal/kg NAR coal at ARA ports fell nearly $15/t from a week earlier to around $115/t, hitting a more than one-month low.

Dutch TTF gas prices fell notably last week. As of June 19, the ICE TTF benchmark Dutch gas futures for July 2026 settled at 42.092 euros/MWh, down 10% from 46.773 euros/MWh a week earlier.

As a transitional month in summer, power plants' procurement momentum weakened significantly after completing earlier restocking, with market activity largely stalling. The news of a U.S.-Iran memorandum of understanding further dampened sentiment, sharply reducing the financial risk premium embedded in energy commodities such as gas, power and coal.

Meanwhile, rising gas storage levels also exerted downward pressure on coal prices. Data showed that EU gas storage levels rose to 45.56% as of June 18, up from 43.36% a week earlier. As coal and gas prices decline, the cost advantage of coal-fired power over gas-fired power is narrowing. While coal remains more economical for now, its future competitive edge will increasingly depend on renewable energy output and weather conditions.

Sumber:

Artikel Lainnya

Liputan 6

Tayang pada

1,76 Juta Metrik Ton Batu Bara Disebar ke 4 PLTU Jaga Listrik di Jawa Tak Padam

Bisnis Indonesia

Tayang pada

10 dari 190 Izin Tambang yang Dibekukan Sudah Bayar Jaminan Reklamasi

IDX Channel.com

Tayang pada

10 Emiten Batu Bara Paling Cuan di 2024, Siapa Saja?

METRO

Tayang pada

10 Negara Pengguna Bahan Bakar Fosil Terbesar di Dunia

CNBC Indonesia

Tayang pada