SXCOAL

Tayang pada

Weekly: Int'l thermal coal market extends weakness, major exporter prices fall

International thermal coal markets remained under pressure over the past week, with prices across major exporting countries broadly declining amid a bearish sentiment. Indonesia saw some domestic supply shift to meet urgent power plant stock needs, but the impact on exports has been limited so far. Prices for coal from South Africa, Australia and Indonesia all fell, with South African high-CV coal hitting a four-month low.

Meanwhile, Chinese buyers maintained cautious purchasing due to high inventories, while India's demand was weak amid the monsoon season and ample domestic coal supply. With demand from the two largest importers simultaneously softening, the seaborne market lost key support. However, power demand in Europe rebounded on hot weather. Overall, weak demand and ample supply coexisted, with geopolitical risk premiums fading and freight rates falling, keeping buyers on the sidelines and offering little prospect for a near-term market recovery.

Supply

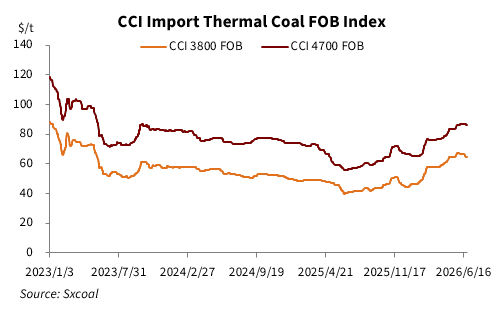

Indonesia The Indonesian thermal coal market remained under pressure over the past week. While some miners diverted supplies to the domestic market to meet power plant needs, overall export supply did not contract significantly, mainly due to weak demand from key buyers. Market participants reported bids for 3,800 Kcal/kg NAR Panamax coal at $65-66/t FOB late last week.

As of June 26, the CCI import 3,800 Kcal/kg NAR thermal coal index was assessed at $64.5/t FOB, down $2/t from a week earlier and $1.4/t from a month earlier. The CCI import 4,700 Kcal/kg NAR index was assessed at $86.5/t FOB, down $0.5/t week on week but up $1.5/t from a month ago.

Indonesia's Ministry of Energy and Mineral Resources recently confirmed that coal exports, which had been diverted to meet domestic demand, have resumed normal shipments. After state utility PLN faced a shortage of high-CV coal for blending at some plants, the government required miners to prioritize domestic market obligations (DMO). A ministry spokesperson said a joint supervisory team has been formed to strengthen DMO enforcement.

Market participants generally believe the policy's actual impact on export volumes is limited. Multiple miners and traders confirmed that only mines under explicit government directives were required to divert supplies to PLN-operated plants, with no widespread export disruptions. Nonetheless, the policy direction has caused some market unease, with some buyers concerned about potential shipment delays.

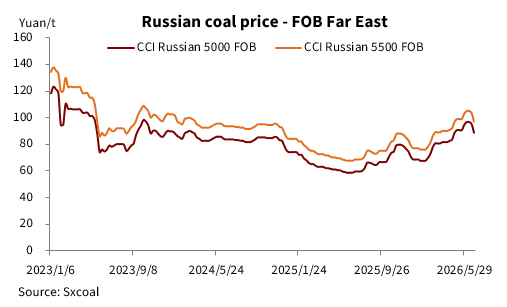

Russia The Russian thermal coal market continued to be affected by weak Asian demand over the past week, with offer prices moving lower. Although Russian coal still holds a price advantage in the Indian market, Indian buyers' willingness to purchase imported coal was low due to monsoon-related demand decline and ample domestic supply, resulting in few actual transactions.

As of June 26, the CCI Russia 5,000 Kcal/kg NAR thermal coal index was assessed at $88.5/t, FOB Far East ports, down $6.5/t from a week earlier and $2/t from a month earlier. The CCI Russia 5,500 Kcal/kg NAR index was assessed at $97/t FOB, down $6.5/t week on week and $2/t month on month.

However, some traders noted that Russian coal still holds a price advantage over coal from Colombia and South Africa, and with normal shipping conditions from Baltic and Black Sea ports, it remains a preferred supplementary source if Indian or Chinese buyers return to the market after further price adjustments.

Australia The Australian thermal coal market remained weak over the past week, with high-CV coal prices falling further due to subdued Asian import demand. As of June 26, the Newcastle 5,500 Kcal/kg NAR thermal coal price continued to decline from the previous week, falling below $95/t FOB, a week-on-week drop of nearly $4/t. The 6,000 Kcal/kg NAR price fell by nearly $5/t from a week earlier to around $133/t.

Market participants noted that buying interest from traditional buyers such as China and South Korea remained low. With shipping through the Strait of Hormuz resuming, buyers in South Korea and Vietnam are refocusing on natural gas alternatives, and additional demand for Australian high-CV coal is gradually returning to normal. A Middle East-based trader said the incremental demand from buyers paying premiums for coal due to geopolitical risks will decrease, as they gradually return to the gas market.

South Africa The South African thermal coal market weakened notably over the past week. As of June 26, the Richards Bay 5,500 Kcal/kg NAR thermal coal price fell below $89/t FOB, down about $1.5/t from a week earlier and over $8/t from a month earlier, hitting a new low since mid-February. The 6,000 Kcal/kg NAR price also fell from the previous week to around $105/t FOB.

Market sources said Indian buyers have almost completely withdrawn from the market, which is the most direct reason for the accelerated price decline. An Indian buyer said the sponge iron industry has largely stopped importing, with buying interest for Indonesian and Australian coal also low, and reliance on domestic coal has increased significantly. A South African miner noted that while freight rates have fallen, they remain relatively high, and Indian direct reduced iron plants can wait for further freight rate declines before re-entering the market.

Market participants believe that with shipping through the Strait of Hormuz resuming, Asian buyers like South Korea, who had switched to coal purchases due to concerns about gas supply disruptions, are gradually returning to the gas market. This normalization of additional demand for high-CV coal has indirectly weighed on South Africa's high-CV coal export outlook.

Demand

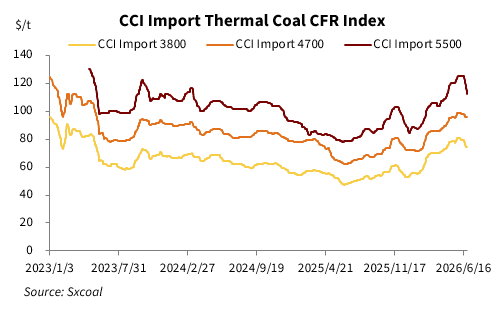

China China's thermal coal import market remained sluggish over the past week, with high port and power plant inventories continuing to suppress buying interest. Although the price advantage of imported coal has widened, it has not effectively stimulated transaction volumes.

As of June 26, the CCI import 3,800 Kcal/kg NAR thermal coal index was assessed at $74.5/t, CFR China southern port, down $4/t from a week earlier. The CCI import 4,700 Kcal/kg NAR index was assessed at $95.5/t CFR, down $2/t week on week. The CCI import 5,500 Kcal/kg NAR index was assessed at $114.5/t CFR, down $9/t from a week earlier.

As of June 28, coal inventory at the six major coastal power groups rose 2.78% from a week earlier to 14.55 million tonnes, with days of consumption remaining at a high level. Although the peak summer season has begun, cooler-than-usual temperatures and above-average rainfall in eastern and southern China have limited the growth in residential cooling power demand, slowing the increase in power plant consumption and curbing restocking enthusiasm.

High power plant inventories, combined with port congestion due to vessel queuing for unloading, have made it difficult for arriving cargoes to be quickly stored. Although the price advantage of imported coal over domestic coal has further widened, it has not spurred large-scale procurement by power plants. Buyers generally expect further price declines and are only making inquiries for essential needs.

India India's thermal coal import demand remained subdued over the past week. Widespread monsoon rains in inland areas have reduced power demand in some regions and eased the urgency for power plant restocking. Meanwhile, ample domestic coal supply with a clear price advantage has further weakened end-users' willingness to purchase imported coal.

Data from India's Central Electricity Authority (CEA) showed that as of June 28, coal inventory at Indian power plants stood at 44.55 million tonnes, down 3.43% from a week earlier. That could cover 14.3 days, down from 14.8 days a week earlier. On that day, 34 power plants were in a critical low-stock state, up by three from the previous week.

Procurement by India's sponge iron and cement sectors has largely stalled. Market sources said that even with continued price declines for imported coal from sources like South Africa, Indian buyers have not returned. During the monsoon season, end-users prefer to consume existing stocks or use cheaper domestic coal, with import procurement limited to price-comparison inquiries for a few low-priced grades, resulting in very few actual transactions.

Market participants said Indian buyers' wait-and-see attitude towards imported coal is unlikely to fade in the near term. With international oil prices and freight rates continuing to weaken, buyers believe future CFR prices have further room to decline and are therefore delaying procurement decisions. Importers are also closely monitoring the impact of subsequent rainfall on domestic coal production and transportation.

Europe The European thermal coal market performed relatively firmly over the past week, mainly due to rising power demand driven by extreme heat. As of late last week, the CIF price for 6,000 Kcal/kg NAR thermal coal at ARA ports rose by about $1/t from a week earlier to over $116/t.

Dutch TTF natural gas prices continued to fall last week. As of June 26, the ICE TTF benchmark Dutch gas futures for July 2026 settled at 40.782 euros/MWh, down 3.11% from 42.092 euros/MWh a week earlier.

Meteorological and power data showed that Europe experienced a heatwave recently. The share of renewable energy in Germany's power generation fell to 61% from 70% a week earlier, while the share of fossil fuel generation rose to 39%. Surging air conditioning demand pushed up overall power load. With wind power output declining and nuclear supply constrained, coal-fired power plants saw a temporary increase in importance as marginal power sources.

However, some market participants believe the recent price rebound is more of a technical correction than a fundamental trend improvement. As of late last week, coal inventory at ARA ports stood at 3.89 million tonnes, still at a relatively high level, up slightly by 50,000 tonnes from a week earlier.

Sumber:

Artikel Lainnya

Liputan 6

Tayang pada

1,76 Juta Metrik Ton Batu Bara Disebar ke 4 PLTU Jaga Listrik di Jawa Tak Padam

Bisnis Indonesia

Tayang pada

10 dari 190 Izin Tambang yang Dibekukan Sudah Bayar Jaminan Reklamasi

IDX Channel.com

Tayang pada

10 Emiten Batu Bara Paling Cuan di 2024, Siapa Saja?

METRO

Tayang pada

10 Negara Pengguna Bahan Bakar Fosil Terbesar di Dunia

CNBC Indonesia

Tayang pada