SX Coal

Tayang pada

Weekly: China's domestic thermal coal market unpinned by import constraints

China's domestic thermal coal market followed a moderately upward trajectory at northern transfer ports last week, partly driven by continued tight availability of supplies from Indonesia and the resulting price rallies in seaborne cargoes, which prompted some utilities to pivot inwards and encouraged domestic sellers to raise offers. The mine-mouth market was mixed at the start of last week, but gained positively approaching the end.

Indonesian low-CV coal prices gained ground further due to supply contraction, as some mines reportedly halted spot coal exports while waiting for more clarity in their RKAB mining quotas for 2026. This also pushed up prices of high-CV coals in the seaborne market.

Sxcoal CCI Index

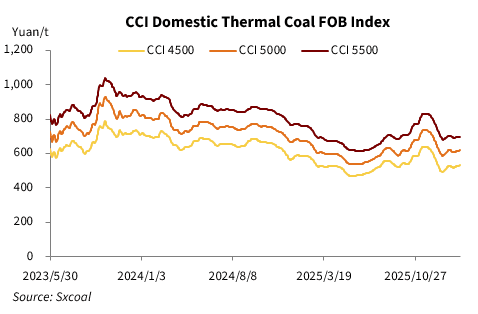

On February 6, the CCI index for 5,500 Kcal/kg NAR domestic spot coal stood at 698 yuan/t FOB northern China port with VAT, rising 2 yuan/t week on week, while the CCI index for 5,000 Kcal/kg NAR domestic coal was up 3 yuan/t from a week earlier to 617 yuan/t.

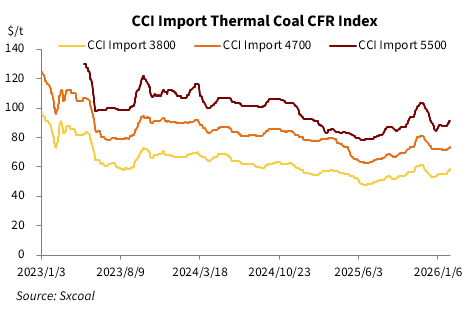

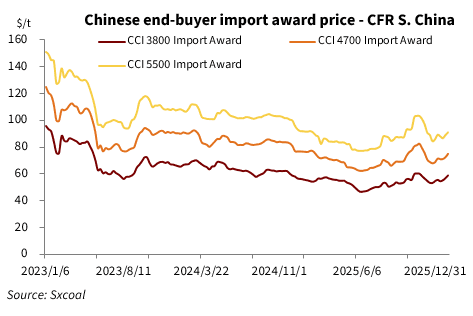

On the same day, the CCI 5500 Import index stood at $91.5/t, CFR southern China port, climbing $2.5/t compared with the previous week. The CCI 4700 Import index was up $1.0/t to $73.5/t, and the CCI 3800 Import index also gained by $1.5/t to $58.5/t.

Weekly Dynamic

Production areas saw prices fluctuate within a narrow range last week, as both supply and demand weakened approaching the Chinese New Year (CNY) holiday.

While a few private mines suspended operations last week, tightening regional supply, the number of major mines closing for holidays remained limited, resulting in only a modest overall decline.

The average capacity utilization of Sxcoal-surveyed mines in Shanxi, Shaanxi, and Inner Mongolia inched lower by 1.06 percentage points from the previous week to 88.7% during the week ended February 4. Their output also fell 1.18% on the week to 16.17 million tonnes. Their coal inventory gained slightly by 0.10% to 4.11 million tonnes.

On the demand side, spot coal purchases remained inactive, as some end users and traders entered holiday mode. Most miner sources reported moderate sales, keeping prices rangebound. Still, pre-holiday restocking demand from certain sectors, such as chemical plants, and from rail station-based traders, was still heard. This boosted sales at a handful of mines offering more competitive prices, resulting in lower inventories and marginally upward price corrections.

Data showed that 21 out of the surveyed 160 thermal coal mines cut prices by 24.7 yuan/t averagely over January 29-February 4, compared with 22 mines lowering prices by 23.22 yuan/t a week earlier; 30 mines raised prices by 16.2 yuan/t, compared to 26 mines hiking prices by 24.2 yuan/t a week ago. The remaining 109 mines kept prices flat.

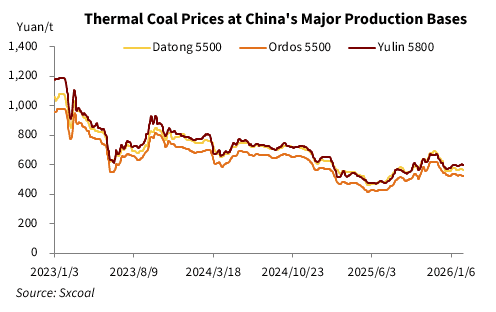

On February 6, Sxcoal assessed Yulin 5,800 Kcal/kg NAR thermal coal at 598 yuan/t, mine-mouth with VAT, rising 2 yuan/t from the preceding week; Ordos 5,500 Kcal/kg NAR coal fell 10 yuan/t to 522 yuan/t; and Shanxi Datong 5,500 Kcal/kg NAR coal was assessed at 567 yuan/t, dipping 1 yuan/t from the previous week.

Some participants noted that with both upstream and downstream sectors gradually shutting down for the holiday, the market is expected to move into a soft pattern, with prices likely to fluctuate within a narrow range.

Portside market held firm to slightly stronger levels last week, even though most end users had completed pre-holiday restocking. This was partly buoyed by talks of suspension of spot coal exports from some Indonesian coal miners following spreading talks regarding sharp cuts on their production quotas this year.

Meanwhile, continued inventory drawdown and the emerging price advantage of portside cargoes compared with seaborne import supplies slightly fueled positive sentiment at Bohai-rim ports.

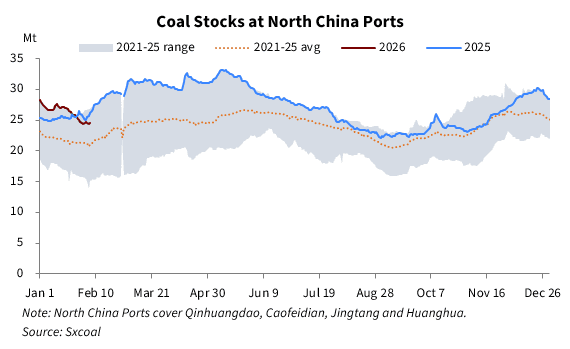

Sxcoal's data showed that on February 6, the combined inventories at Qinhuangdao, Jingtang, Caofeidian, and Huanghua ports totaled 24.50 million tonnes, down 0.74% from the previous week and 8.83% month on month. It also fell below the year-ago level by 6.14%.

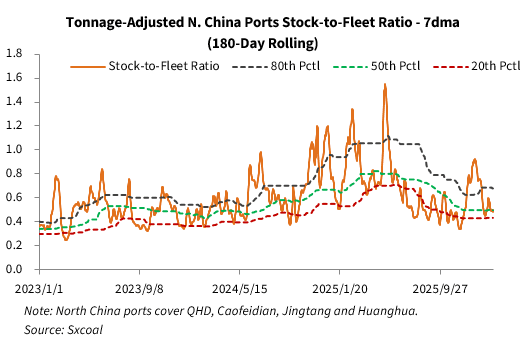

The tonnage-adjusted stock-to-fleet ratio, a major gauge for on-sight supply at northern ports, dipped marginally to 0.48 on February 6, falling slightly below the six-month rolling 50th percentile yet still above the 20th percentile, according to Sxcoal's assessment, indicating a slightly further tightening of supply at the port market.

The decline was ascribed to weak rail coal supply to northern ports, as supply contracted and some traders entered holidays early. Coal deliveries through Daqin railway, a major transport artery connecting production areas to northern ports, dipped by 1.9% week on week to 1.02 million tonnes during the week ended February 6. China Railway Hohhot Group, which supervises the rail networks in central and western Inner Mongolia, approved 26 trains to transport coal each day on average last week, up 10 from a week earlier.

Demand from power plants was too modest to provide any meaningful support. Data showed that coal consumption at inland power plants, which mainly rely on domestic resources, retreated by 18.1% week on week and 15% on the month as of February 4, following the recent rebound in temperatures.

However, anticipating supply constraints in Indonesia to sustain in the near term, some participants turned more optimistic about the post-holiday outlook, prompting a small pickup in speculative buying and pushing portside prices gradually higher.

Yet some sources warned that the underlying demand support remained limited, making it difficult for prices to extend gains. Attention is expected to focus on post-holiday port inventory changes, the pace of resumption across the supply chain, and whether Indonesian supply tightness sustains.

Hydropower generation remained fluctuating. Sxcoal's data showed that water outflow through the Three Gorges dam, a key indicator of China's hydropower generation, increased by 0.4% from a week ago to 8,010 cu.m/s on February 6. That climbed 7.4% from the preceding month, yet still fell 5.3% compared with the preceding year.

Import market Indonesian thermal coal prices rose further last week, as some local miners reportedly suspended spot coal exports amid talks of a sharp reduction of the approved RKAB mining quotas this year, with some ranging 40-70%, which, though, was denied by the country's energy ministry later.

The Ministry of Energy and Mineral Resources (ESDM) of Indonesia signaled lately that the RKAB for coal this year would be slightly above 600 million tonnes but well below the realized production of 790 million tonnes in 2025.

Meanwhile, in order to ensure ample supply to the domestic end users, the ministry is preparing to increase the mandatory domestic market obligation, or DMO, for coal to more than 30% from the previous 25% to guarantee domestic supply. If these two policies come into effect, export supply is anticipated to be significantly reduced in the following several months.

FOB offers for Indonesian 3,800 Kcal/kg NAR coal on Panamax vessels were heard at a $3-5/t premium to the index. One major Chinese utility reportedly bought three cargoes of the same-CV coal from Indonesia at prices of 458-463 yuan/t CFR China with VAT on February 4, with the lowest netting back to around $51.9/t FOB East Kalimantan on a Panamax basis.

On February 6, Sxcoal assessed the utility tender-winning prices for 3,800 Kcal/kg NAR coal at 460 yuan/t CFR South China with VAT, rising 15 yuan/t compared with 445 yuan/t in the preceding week.

Indonesian low-CV coal lost its price advantage following fast rallies. Sxcoal's calculation showed on February 6 that Indonesian 3,800 Kcal/kg NAR coal was 3.22 yuan/t expensive compared with domestic 4,500 Kcal/kg NAR coal on a CV-adjusted and delivered-to-South China basis, compared with an 8.17 yuan/t advantage in the week prior.

High-CV 5,500 Kcal/kg NAR imported coal from Australia was also buoyed by tight Indonesian cargo availability. Australian 5,500 Kcal/kg NAR coal was assessed 3.6 yuan/t cheaper compared with the domestic 5,500 Kcal/kg NAR coal on a landed basis, narrowing sharply by 21.40 yuan/t week on week.

Forecast

China's domestic thermal coal prices are likely to stay rangebound during the week before the CNY holiday, considering weak yet balanced supply-demand fundamentals. The seaborne import market is anticipated to keep inching up due to the supply-side constraints, yet the overall upward room could be limited by the holiday slowdown in China.

Sumber:

Artikel Lainnya

Liputan 6

Tayang pada

1,76 Juta Metrik Ton Batu Bara Disebar ke 4 PLTU Jaga Listrik di Jawa Tak Padam

Bisnis Indonesia

Tayang pada

10 dari 190 Izin Tambang yang Dibekukan Sudah Bayar Jaminan Reklamasi

IDX Channel.com

Tayang pada

10 Emiten Batu Bara Paling Cuan di 2024, Siapa Saja?

METRO

Tayang pada

10 Negara Pengguna Bahan Bakar Fosil Terbesar di Dunia

CNBC Indonesia

Tayang pada