SX Coal

Tayang pada

Monthly: int'l thermal coal prices rise in Feb on tightening supply

The international thermal coal prices rose in February, supported mainly by tightening supply across major exporting countries, which pushed the overall price benchmark notably higher from February levels.

Coal producers in several key exporting nations faced varying degrees of production and logistics constraints during the month. At the same time, Indonesia's move to cut its coal output target fueled expectations of tighter supply, lending further support to seaborne coal prices.

However, demand across major importing countries remained relatively subdued. In China, procurement appetite was muted due to the Lunar New Year holiday and seasonally weak demand from non-power sectors after the holiday period. India maintained purchases to meet basic consumption needs, but ample domestic inventories reduced the urgency for imports.

By contrast, some overseas buyers remained relatively active and showed greater willingness to accept higher prices. Overall, the global thermal coal market in February was characterized by a tug-of-war between tightening supply and cautious demand, with prices maintaining a firm trend.

Supply Side

Australia In February, Australia's thermal coal market faced supply constraints, while bullish sentiment in the seaborne market pushed prices for high-CV coal higher.

As of February 27, 5,500 Kcal/kg NAR thermal coal at Newcastle port stood at $86.65/t, up 14.15% or $10.74 from the end of January, hitting a new high since mid-November.

Earlier in the month, heavy rain and flooding disrupted operations at some mines and rail networks in Queensland. Although the scale and duration of the disruptions were less severe than in January, they still created short-term supply disturbances.

Over the month, Australian export shipments fluctuated considerably, with dispatch volumes dropping sharply in early February. Producers prioritized long-term contracts, leaving spot market liquidity limited and providing support for prices, particularly for high-CV thermal coal.

Meanwhile, buyers in India and other Asian countries continued to show interest in inquiries for high-quality Australian coal, though purchasing activity remained cautious amid elevated offer prices.

Indonesia Indonesia's Ministry of Energy and Mineral Resources (ESDM) adjusted up most of its benchmark coal reference prices or the HBAs (Harga Batubara Acuan) for H1 of February, yet lowered them for H2.

The HBA for 6,322 Kcal/kg GAR coal was set at $106.11/t in H1 and $102.87/t in H2. The HBA I, gauging 5,300 Kcal/kg GAR, was priced at $73.96/t in H1 and $71.74/t in H2, while the HBA II, measuring 4,100 Kcal/kg GAR, was set at $48.21/t in H1 and $47.34/t in H2. The HBA III, basis 3,400 Kcal/kg GAR, was set at $35.83/t and $33.85/t, respectively.

In February, expectations of tighter supply in Indonesia continued to intensify as the government's coal output control policies took effect. While several large mines had their 2026 RKAB approved, many smaller producers were still awaiting RKAB approvals, raising concerns about forward spot supply.

Seasonal factors also weighed on output. February falls within Indonesia's rainy season, with frequent rainfall in key producing regions such as Kalimantan disrupting mining operations and barge transportation. In addition, the start of Ramadan further reduced production and shipping efficiency at some mines.

Against this backdrop of tightening supply expectations and operational constraints, Indonesian miners showed strong resistance to lowering prices. Many prioritized fulfilling long-term contracts and significantly reduced spot market offers, leaving the availability of low- to mid-CV coal increasingly tight.

At the same time, the government continued to enforce its Domestic Market Obligation (DMO) policy to ensure sufficient coal supply for local power generation, which could further limit volumes available for export.

Supported by these factors, Indonesian thermal coal FOB prices rebounded steadily during February. On February 28, the CCI index for Indonesian 3,800 Kcal/kg NAR coal stood at $57.7/t FOB, rising $10.2/t from the previous month; the CCI Import 4700 index stood at $76.5/t FOB, up $11/t month on month.

South Africa South African thermal coal prices recorded notable gains in February, supported by persistent rail logistics constraints that continued to limit exports. As of February 27, South African 5,500 Kcal/kg NAR thermal coal prices stood at $88.61/t, up $7.54/t or 9.3% from the end of January. Prices briefly climbed above $89/t during the month, the highest level since late November 2024.

South Africa's coal exports remained constrained by longstanding rail bottlenecks, while periodic fluctuations in transport capacity further affected cargo circulation.

Although stockpiles at the Richards Bay Coal Terminal (RBCT) fluctuated in the month, overall export was largely determined by rail performance. In early February, weekly shipments from the terminal fell by around 40% from the previous week.

Despite these constraints, steady demand from India, particularly from sponge iron producers, provided key support to the market. Supply uncertainties in alternative sources such as Indonesia and Australia encouraged Indian buyers to increase enquiries for South African cargoes, helping push prices higher through the month.

Data from the country's customs showed its thermal coal (bituminous and sub-bituminous) exports reached 6.07 million tonnes (Mt) in December 2025, down 6.42% year on year (YoY) and 3.04% month on month (MoM). RBCT shipments totaled 5.89 Mt, a fall of 4.46% YoY and down 2.92% MoM.

Russia In February, Russian coal exports tightened further due to export transportation bottlenecks and Middle East conflicts.

As of February 27, Sxcoal assessed Russian 5,000 Kcal/kg NAR thermal coal at $77.5/t FOB Far East ports, up $10/t month on month; Russian 5,500 Kcal/kg NAR coal was assessed at $86/t, up $10/t from a month earlier.

The Baltic Sea experienced its most severe ice conditions in 15 years, significantly disrupting vessel movements at Ust-Luga Port and St. Petersburg Port. Non-ice-class vessels were prohibited from entering, while other ships could only access the ports under the escort of icebreakers, often on a single-vessel basis.

This directly affected the pace of Russian coal exports to Europe, Turkey and even India. Market participants warned that coal shipments from several major Baltic terminals could face interruption risks.

Meanwhile, Taman Port, located in the Sea of Azov, was hit by a Ukrainian drone attack in mid-February, damaging port infrastructure. The port handles more than 1 million tonnes of coal exports per month, and the incident further heightened market concerns over potential disruptions to Russian supply.

Although Russian experts expected total coal exports to remain at 195–200 million tonnes in 2026, the combined impact of logistics constraints and unexpected disruptions in February caused Russian spot coal exports to stagnate.

Kpler data showed Russia's seaborne coal exports totaled 10.16 Mt in January 2025, down 16.28% YoY and 26.67% MoM. Of this, thermal coal exports reached 7 Mt, falling 15.86% YoY and 24.52% MoM.

Demand Side

China China's imported thermal coal market remained buoyant in February, with prices trending steadily higher. In early February, purchasing activity slowed as most market participants had already completed pre-holiday restocking ahead of the Chinese New Year. Meanwhile, power plants' inventories stayed at relatively high levels, while coal burns declined as the holiday approached, reducing tender demand from utilities.

By February 28, coal inventories at the six major coastal power plants reached 13.67 Mt, up 4.03% from the prior month. Daily coal burn averaged at 685,000 tonnes, a 2.06% fall MoM and down 15.62% YoY. The coal stockpiles enough for 20 days' consumption.

After the holiday, although industrial enterprises gradually resumed operations, electricity consumption entered its traditional seasonal lull. Coal burns at coastal utilities recovered slowly, while inventories remained above safety levels, with stock coverage generally exceeding 16 days, limiting large-scale spot purchases.

Non-power end users also resumed operations at a relatively slow pace, keeping procurement demand subdued.

Nevertheless, tighter domestic supply due to holidays and firm sentiment in overseas markets, and rising seaborne freight rates, kept imported coal costs elevated.

By the end of the month, imported coal prices had risen significantly compared with early February.

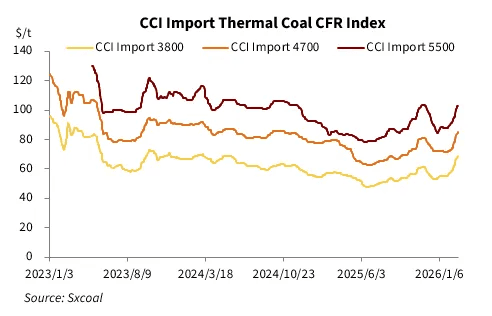

As of February 28, the 3,800 Kcal/kg NAR imported coal was $67.5/t CFR southern China, a $12/t increase from the end of January. The 4,700 Kcal/kg NAR coal was offered $83.5/t, up $12/t from the previous month. The 5,500 Kcal/kg NAR coal was $102.5/t, up $14.5/t.

As of the end of February, imported 3,800 Kcal/kg NAR coal was 14.81 yuan/t cheaper than the equivalent domestic grade, compared with 20.06 yuan/t at the end of January. The price gap between 4,700 Kcal/kg NAR cargoes and domestic equivalent narrowed to 21.84 yuan/t from 46.64 yuan/t a month earlier.

Japan and S Korea In January, Japan's thermal coal imports (including other bituminous coal and other coal) reached 9.89 Mt, down 4.62% YoY but up 5.89% MoM. Of this, imports of other bituminous coal were 9.1 Mt, down 5.82% YoY but up 6.87% MoM; imports of other coal stood at 0.79 Mt, up 11.7% YoY but down 4.2% MoM.

South Korea imported 8.78 Mt of thermal coal in January, rising 27.12% YoY and 39.2% MoM. The country included 8.52 Mt of other bituminous coal, up 26% YoY and 39.86% MoM, while imports of other coal totaled 261,300 tonnes, jumping 78.74% YoY and 20.88% MoM.

India In February, India's demand for imported thermal coal remained weak. On the one hand, coal inventories at Indian power utilities remained ample. Data from the Central Electricity Authority (CEA) showed that as of February 24, coal inventories at Indian power utilities stood at 58.98 Mt, up 8.3% MoM, enough for 19.22 days of usage, compared with 17.8 days at the end of January.

On the other hand, industrial demand from non-power sectors such as sponge iron and cement provided some support to the market. These users continued to inquire about mid- to high-CV coal from South Africa, the United States and Russia, with industrial buyers maintaining relatively stable procurement volumes of South African coal in particular.

However, rising freight rates and fluctuations in the rupee exchange rate limited buyers' willingness to accept higher prices, leading many to adopt a hand-to-mouth purchasing strategy.

Notably, reports indicated that the Indian government is seeking to cut coal imports for power plants by at least 30% in 2026. While this policy expectation had no direct impact on the market during the month, it has introduced additional uncertainty to the longer-term outlook for India's seaborne coal demand.

According to the Indian Ports Association (IPA), India's 12 major state-owned ports imported 16.66 Mt of coal in January 2025, down 2.2% YoY but up 1.95% MoM. Of this, thermal coal imports were 11.03 Mt, down 0.38% YoY but up 15.1% MoM.

India's power producers imported 3.63 million tonnes of thermal coal in the month, up 5.88% month on month but down 11.6% from a year ago, showed data from the Central Electricity Authority (CEA). Among all the coal imported by power companies, 3.13 million tonnes were directly burned, while 494,000 tonnes were blended with domestic coal.

Sumber:

Artikel Lainnya

Liputan 6

Tayang pada

1,76 Juta Metrik Ton Batu Bara Disebar ke 4 PLTU Jaga Listrik di Jawa Tak Padam

Bisnis Indonesia

Tayang pada

10 dari 190 Izin Tambang yang Dibekukan Sudah Bayar Jaminan Reklamasi

IDX Channel.com

Tayang pada

10 Emiten Batu Bara Paling Cuan di 2024, Siapa Saja?

METRO

Tayang pada

10 Negara Pengguna Bahan Bakar Fosil Terbesar di Dunia

CNBC Indonesia

Tayang pada