SX Coal

Tayang pada

Monthly: int'l thermal coal market swings in Jun, ends lower

International thermal coal prices swung sharply in June, with an initial rally driven by geopolitical tensions giving way to broad declines as supply disruptions eased and demand from top importers China and India weakened.

The market surged in early June on a combination of factors including supply disruptions in Colombia, heightened Middle East tensions and strong summer demand expectations. But the risk premium quickly evaporated after a US-Iran memorandum of understanding was reached and the Strait of Hormuz reopened to shipping, cooling speculative buying.

On the demand side, China's buying remained sluggish due to high port and power plant inventories and above-average rainfall in the south, while India stayed on the sidelines amid the monsoon season and ample domestic coal supply. The absence of the two largest importers left the seaborne market without key support, keeping fundamentals weak.

Australia

Australian thermal coal prices followed a clear up-then-down trajectory in June. By June 26, the Newcastle 5,500 Kcal/kg NAR price had fallen below $95/t, down over $8/t or 9.2% from end-May. The price briefly touched nearly $105/t during the month, a fresh high since late October 2023.

The early-month rally was driven by escalating Middle East conflict, rising European prices and tightening Indonesian high-CV coal supply. Sentiment reversed sharply in the second half of the month as geopolitical tensions eased, Chinese demand cooled and high domestic power plant inventories and port congestion dampened importers' appetite for forward cargoes.

Notably, a sharp drop in Capesize freight rates made Newcastle 5,500 Kcal/kg coal more price-competitive relative to 6,000 Kcal/kg grades, prompting some Japanese and Korean buyers to switch to the lower-CV grade for cost efficiency.

While ongoing mine safety inspections in China, lingering supply uncertainty in Indonesia and the approaching peak summer power demand in North Asia limited downside, market participants widely expected the resumption of Strait of Hormuz shipping to reduce incremental demand from buyers who had paid a geopolitical risk premium. A gradual shift back to natural gas was also seen weakening additional demand support for Australian high-CV coal.

Indonesia

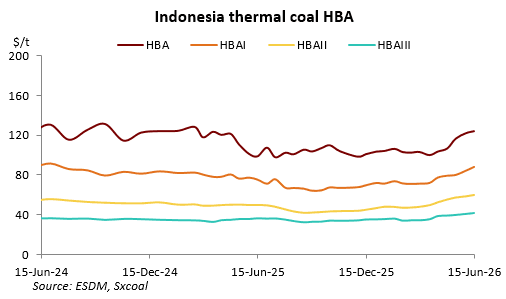

Indonesia's Ministry of Energy and Mineral Resources raised its HBA reference prices for both the first and second halves of June, with medium- and high-CV grades seeing more pronounced increases.

The HBA for coal with a gross calorific value of 6,322 Kcal/kg (12.26% moisture, 0.66% sulfur, 7.94% ash) was set at $121.83/t for the first half of June and $123.91/t for the second half, serving as the benchmark for 6,100-6,500 Kcal/kg coal.

The HBA I for 5,300 Kcal/kg GAR coal (21.32% moisture, 0.75% sulfur, 6.04% ash) was $84.53/t in the first half and $88.4/t in the second half, covering the 5,100-5,500 Kcal/kg range.

The HBA II for 4,100 Kcal/kg GAR coal (35.73% moisture, 0.23% sulfur, 3.90% ash) was $58.81/t in the first half and $60.19/t in the second half, for the 3,900-4,300 Kcal/kg range.

The HBA III for 3,400 Kcal/kg GAR coal (44.3% moisture, 0.24% sulfur, 3.88% ash) was $40.32/t in the first half and $41.19/t in the second half, for the 3,200-3,600 Kcal/kg range.

Indonesian thermal coal markets remained significantly affected by policy uncertainty in June. The transition period for the government's new state-owned entity, Daya Anagata Nusantara Resources (DSI), to strengthen oversight of exports of strategic resources including coal officially began on June 1.

Although officials clarified that DSI's role is to monitor prices rather than replace exporters, policy uncertainty combined with delays in approving RKAB production quotas led miners to adopt a conservative approach to spot sales, keeping medium- and high-CV supply tight.

In late June, to fill an annual coal supply gap of around 20 million tonnes for state utility PLN, the government required some miners to prioritize domestic market obligations (DMO) and divert supplies to domestic power plants, briefly raising concerns about export disruptions. While officials later confirmed exports had resumed, the episode reinforced market doubts about the flexibility of Indonesian coal exports.

Meanwhile, delays in RKAB production quota approvals continued to constrain spot supply, with some miners having exhausted their annual quotas and awaiting government revisions to second-half production plans. Miners widely reported that even if the government raises RKAB output targets, the approval process would take until late July or August, making it difficult to generate effective incremental supply in the near term. This kept miners' offer premiums high and medium- and high-CV supply persistently tight.

Indonesian thermal coal FOB prices were stable to slightly lower from end-May. Sxcoal's CCI index showed Indonesian 3,800 Kcal/kg NAR coal at $64.5/t FOB as of June 30, down $2.9/t month on month, while 4,700 Kcal/kg NAR coal was flat at $86.5/t.

South Africa

South African thermal coal prices fell in a one-sided decline in June due to weak demand support. By June 26, the 5,500 Kcal/kg NAR price had fallen below $90/t, down over $7/t or 7.5% from end-May.

Demand from traditional buyer India remained subdued. Ample domestic coal production, the approaching monsoon season reducing procurement urgency, and weak interest from the sponge iron sector due to falling finished steel prices all weighed on South African coal shipments.

Despite high stockpiles at the Richards Bay Coal Terminal (RBCT) and a derailment in early June that briefly affected rail transport, these supply-side disruptions provided virtually no price support amid weak demand.

South African customs data showed April 2026 thermal coal (bituminous and sub-bituminous) exports at 6.55 million tonnes, up 5.1% year on year but down 7.21% from March. RBCT thermal coal exports in April stood at 6.29 million tonnes, up 6.57% year on year but down 6.86% month on month.

Russia

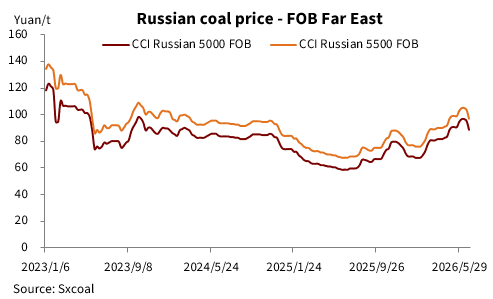

Russian thermal coal prices also rose then fell in June, with the overall price level shifting significantly lower by month-end. Performance varied by coal grade due to regional demand divergence.

As of June 26, CCI Russian 5,000 Kcal/kg NAR coal at Far East ports was $88.5/t FOB, down $6/t from a month earlier, while CCI Russian 5,500 Kcal/kg NAR coal was also down $6/t to $97/t.

In early June, amid uncertainty over Indonesian export prospects, Russian coal gained favor among Asian buyers due to its price advantage, with Far East port high-CV prices rising alongside the global market. However, as demand from key Asian buyers China and India cooled, Russian coal offers came under pressure in the second half of the month, with Far East port high-CV FOB quotes falling notably from mid-month highs.

Kpler vessel tracking data showed Russia's total seaborne coal exports in May 2026 at 13.76 million tonnes, down 7.85% year on year and 4.89% month on month. Seaborne thermal coal exports totaled 10.34 million tonnes, down 3.64% year on year but up 9.09% from April.

China

China's thermal coal import market showed a clear "peak season without peak demand" pattern in June, becoming a key factor driving the Asia-Pacific price decline in the second half of the month.

Despite widespread expectations of El Nino bringing hot weather, actual temperatures in eastern and southern China were cooler than normal, with above-average rainfall boosting hydropower output and significantly curbing thermal power demand.

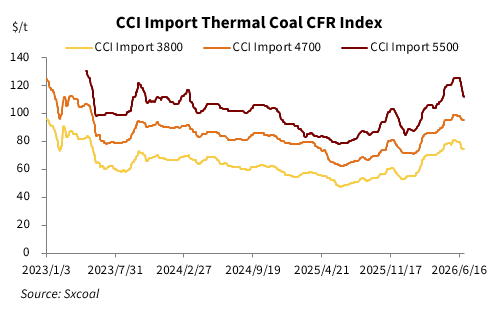

As of June 30, the CCI index for imported 3,800 Kcal/kg NAR coal at southern China ports were $74.5/t CFR, down $6.5/t from end-May. Imported 4,700 Kcal/kg NAR coal was $95.5/t, down $3/t, while 5,500 Kcal/kg NAR coal was $112.5/t, down $12.5/t.

Coastal power plant coal inventories continued to rise and remained at historically high levels for the period, with days of consumption coverage staying above safe levels, suppressing utilities' spot procurement appetite.

As of June 30, coal inventories at the six major coastal power groups totaled 14.66 million tonnes, up 9.08% from end-May. Daily consumption was 756,000 tonnes, down 6.67% month on month but up 3.86% year on year, with inventory coverage rising to 19 days.

Port inventories also remained elevated, with earlier concentrated arrivals of imported coal causing severe congestion at southern China ports, where unloading waiting times reached up to two weeks. This increased demurrage costs and prevented the price advantage of imported coal over domestic coal from translating into effective transaction volumes.

At end-June, imported 3,800 Kcal/kg NAR thermal coal was 572.46 yuan/t CFR with VAT, down 49.03 yuan/t from 621.49 yuan/t at end-May. The imported 4,700 Kcal/kg NAR coal was 733.82 yuan/t, down 21.94 yuan/t from 755.76 yuan/t.

As of end-June, imported 3,800 Kcal/kg NAR coal at southern China ports was 8.26 yuan/t higher than domestic coal of the same quality, narrowing from 11.41 yuan/t at end-May. The price spread for imported 4,700 Kcal/kg NAR coal was 9.16 yuan/t, narrowing significantly from a 32.94 yuan/t discount a month earlier.

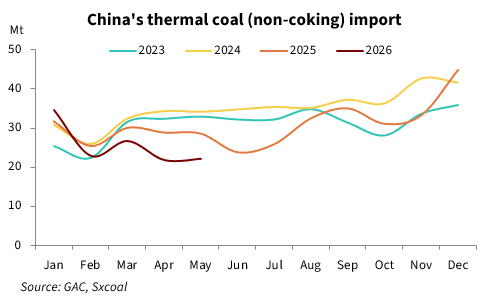

Customs data showed China's May thermal coal (non-coking coal) imports at 22.12 million tonnes, down 22.8% from 28.65 million tonnes a year earlier but up 1.55% from 21.78 million tonnes in April.

The value of May thermal coal imports was $1.63 billion, down 15.12% year on year, implying an average import price of $73.67/t, up $6.66/t from a year earlier.

Japan and Korea

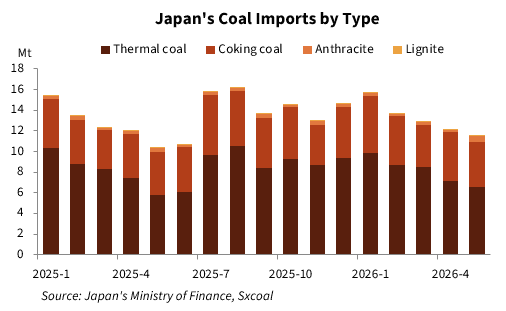

Japan's May thermal coal imports (including other bituminous coal and other coal) totaled 6.6 million tonnes, up 14.1% year on year but down 7.05% from April. Imports of other bituminous coal were 6 million tonnes, up 10.05% year on year but down 6.32% month on month. Imports of other coal were 598,700 tonnes, up 80.67% year on year but down 13.78% month on month.

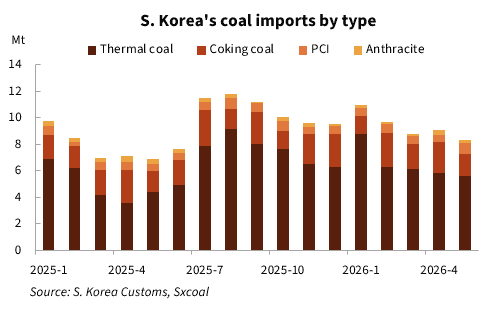

South Korea's May thermal coal imports (other bituminous coal and other coal) were 5.59 million tonnes, up 25.67% year on year but down 4% from April. Imports of other bituminous coal were 5.37 million tonnes, up 27.65% year on year but down 4.32% month on month. Imports of other coal were 212,300 tonnes, down 9.75% year on year but up 5.12% month on month.

India

Indian buyers remained largely absent from the imported thermal coal market in June. Despite the arrival of peak summer power demand, strong domestic coal production and improved logistics allowed end-users to easily access cheaper domestic coal.

At the same time, widespread monsoon rains reduced both power demand and the urgency for power plants to replenish inventories. Indian power plant coal inventory coverage remained at safe levels.

Data from the Central Electricity Authority (CEA) showed that as of June 29, total coal inventories at Indian power utilities stood at 44.34 million tonnes, down 9.54% from end-May. Inventory coverage was 13.2 days, down from 14.8 days at end-May.

Non-power sectors such as sponge iron and cement also reduced purchases of imported coal, particularly South African grades, due to weak product prices. The market widely expected that large-scale Indian buyer return was unlikely before the monsoon season fully ended.

Data from the Indian Ports Association (IPA) showed that India's 12 major state-run ports handled 18.69 million tonnes of coal imports in May 2026, up 10.24% year on year and 8.43% month on month. Thermal coal imports accounted for 12.31 million tonnes, up 6.84% year on year and 3.41% month on month.

CEA data showed Indian power utilities imported a total of 4.08 million tonnes of coal in May 2026, down 25.76% year on year but up 16.29% month on month, the highest since July 2025. Of the total, 3.66 million tonnes were for plants using imported coal exclusively, while 417,700 tonnes were for blending with domestic coal.

Sumber:

Artikel Lainnya

Liputan 6

Tayang pada

1,76 Juta Metrik Ton Batu Bara Disebar ke 4 PLTU Jaga Listrik di Jawa Tak Padam

Bisnis Indonesia

Tayang pada

10 dari 190 Izin Tambang yang Dibekukan Sudah Bayar Jaminan Reklamasi

IDX Channel.com

Tayang pada

10 Emiten Batu Bara Paling Cuan di 2024, Siapa Saja?

METRO

Tayang pada

10 Negara Pengguna Bahan Bakar Fosil Terbesar di Dunia

CNBC Indonesia

Tayang pada