SXCOAL

Tayang pada

Monthly: China Jun thermal coal prices in inverted V-shape amid volatile demand

China's domestic thermal coal prices in June traced a rise-stabilization-decline trajectory. Prices edged up earlier the month backed by accident-induced supply disruptions and growing coal consumption at coastal power plants. After mid-June, however, persistent rainfall dragged down coal burns. This, combined with elevated fuel stocks at power plants, modestly pressed down coal prices by the month end.

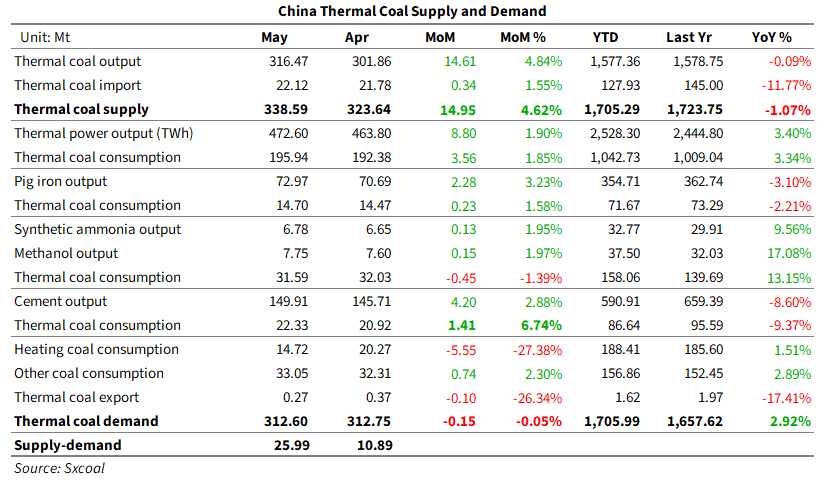

May supply-demand summary

Supply China's total thermal coal supply stood at 338.59 million tonnes in May, rising 4.62% month on month. Cumulative supply in January-May stood at 1.71 billion tonnes, down 1.07% year on year.

Demand Thermal coal consumption totaled 312.60 million tonnes in May, down 0.05% from a month earlier. Demand over January-May reached 1.71 billion tonnes, increasing 2.92% on the year.

Overall, the market recorded a supply surplus of 25.99 million tonnes, higher than 10.89 million tonnes in April.

Production areas

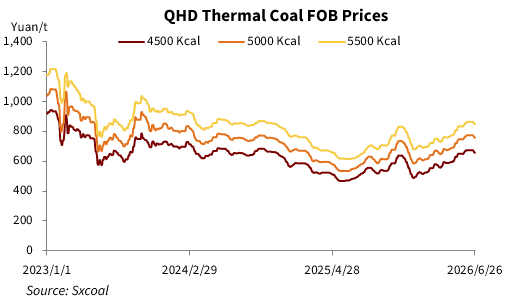

Thermal coal prices across China's major producing regions were range-bound last month. In the first half, ongoing safety inspections kept overall coal supply constrained, and the demand side performed relatively well. Power plants steadily fulfilled long-term contracts, and chemical plants consistently made essential restockings, jointly fueling price upticks. However, mine-mouth prices softened subsequently as portside prices stagnated and then weakened.

On the supply front, a coal mine accident in Shanxi's Changzhi triggered stricter safety inspections across top coal-producing regions including Shanxi, Shaanxi, and Inner Mongolia. Several mines were forced to halt or cap operations, lowering overall capacity utilization rates. Sxcoal's tracking data showed the average weekly output of surveyed mines in the month to June 24 stood at 15.87 million tonnes, down 5.3% month on month and 3.7% on the year.

Reductions in both portside thermal coal prices and in third-party coal buy prices from a major miner prompted more traders and washing plants to adopt a wait-and-see sentiment. Some miners hence reported poor offtakes and marginal stock builds. Yet, overall coal inventories hovered low, and miners faced minimal sales pressure. As of June 24, stocks at Sxcoal-surveyed mines stood at 3.91 million tonnes, down 0.3% from a month earlier and 9.1% lower year on year.

As of June 26, Shanxi Datong 5,500 Kcal/kg NAR thermal coal was assessed at 715 yuan/t, mine-mouth with VAT, down 3 yuan/t from a month earlier. Inner Mongolia Ordos 5,500 Kcal/kg NAR coal was at 622 yuan/t, advancing 27 yuan/t from the month before, and Shaanxi Yulin 5,800 Kcal/kg NAR thermal coal was assessed at 700 yuan/t, rising 13 yuan/t month on month.

Transfer ports

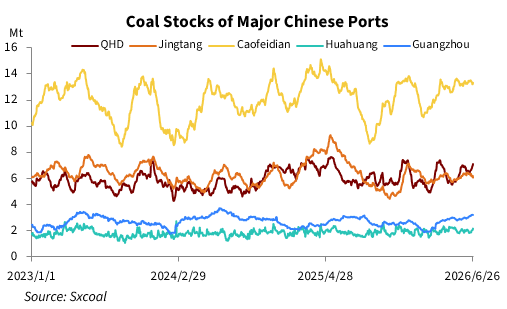

Coal inventories at northern transfer ports ramped up in June. On the inflow side, resources under long-term contracts continued to arrive at ports. However, railway station-based traders eased port-bound coal shipments due to muted transactions. This, together with constrained mine-mouth supplies and persistent difficulties in securing rail wagon approvals, further eroded traders' shipping enthusiasm, thereby slightly decreasing portside intakes.

In terms of outflows, some end users modestly increased restocking approaching the peak summer. Overall, inflows and outflows were largely balanced, leaving portside inventories lingering high.

As of June 29, total inventories at major northern ports stood at 28.66 million tonnes, up 0.35% month on month and 3.05% year on year. Qinhuangdao port stocks reached 7.08 million tonnes, gaining 1.58% from a month earlier and 23.34% on the year.

Compared to regions along the Yangtze River and eastern and central China, southern regions braced summer earlier, thus increasing thermal coal consumption. Traders secured supplies in anticipation of robust summer demand. Meanwhile, spot imported resources were also sufficient. However, the early arrival of the flood season in the south, marked by prolonged and intense precipitation, depressed coal consumption at power plants. These factors combined to drive coal inventories at Guangzhou port to elevated levels, even causing vessel congestion. Guangdong port inventories reached 3.22 million tonnes as of June 24, up 12.2% on the month and 4.8% on the year.

Supply restrictions post-accident, elevated imported coal prices, and restocking from power plants lifted portside thermal coal prices in early June. However, the market was then trapped in a stalemate due to sustained rainfall in southern China, as well as concentrated arrivals of imported cargoes. Portside prices pulled back by the end of June, weighed down by high inventories across mid- and downstream sectors.

As of June 26, 5,500 Kcal/kg NAR thermal coal traded at Qinhuangdao port reached 851 yuan/t, FOB with VAT, rising 10 yuan/t from the month before.

At southern China's Guangzhou port, Shanxi premium mixed 5,500 Kcal/kg NAR coal with 0.6% sulfur gained 10 yuan/t month on month to 910 yuan/t, ex-stock with VAT. Prices at Guangzhou port tracked the northern port market trend.

Import market

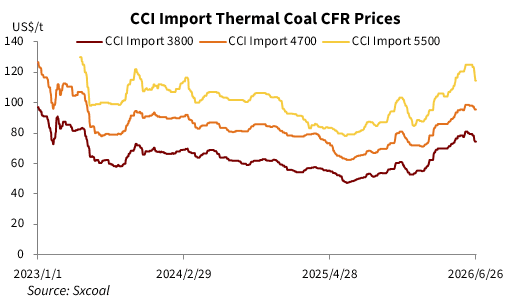

Elevated end-user inventories and ample imported resources, as well as high stocks and longer offloading cycles at southern China ports, prompted some importers to cut bidding prices of tenders to end users. Moreover, easing tensions in the Middle East pressed down crude oil prices, which in turn lowered international seaborne freight rates and reduced import costs. Australian high-CV grades experienced steeper declines than Indonesian low- and mid-CV coal, narrowing the price gap against Chinese equivalents.

As of June 26, the CCI index for imported 5,500 Kcal/kg, 4,700 Kcal/kg, and 3,800 Kcal/kg NAR coal stood at $114.5/t, $95.5/t, and $74.5/t CFR, respectively, falling $7.5/t, $1/t, and $4.5/t from a month ago.

Consuming areas

Coal consumption at coastal power plants retreated during the flood season in June. Affected by peak-summer expectations and concerns over mine-mouth supply constraints, generators actively sought coal under long-term contracts. Combined with imported coal replenishments, fuel inventories at power plants experienced both month-on-month and year-on-year growth.

As of June 26, stocks at power plants under six major coastal power groups stood at 14.26 million tonnes, up 6.46% from end-May and 2.92% year on year. Daily consumption was 782,000 tonnes, down 3.58% month on month and 5.67% year on year. Available days of inventory stood at 18.2 days, 1.7 days higher than a month earlier and also up 1.5 days on the year.

June highlights recap

The follow-up impacts of the Shanxi mine accident persisted, with multiple provinces requiring thorough investigations and rectifications of coal mine safety risks and hidden dangers. Meanwhile, several provincial governors conducted on-site underground safety inspections, underscoring a "top-level supervision" model and the rigorous enforcement of accountability.

Against this backdrop, the central government also moved frequently on coal mine safety during the annual Work Safety Month. The National Mine Safety Administration held a video briefing on June 9, interpreting the newly revised standards for determining major accident hazards at mines and arranging implementation work. On June 25, it issued a guidance opinion and called on mines to further focus on the core goal of preventing accidents and strengthen the implementation of production safety responsibility.

In addition, coal supply assurance drew heightened attention in the run-up to the peak summer. At a National Development and Reform Commission press conference on June 18, spokesperson Li Chao addressed market concerns that stringent safety inspections and rising coal prices might exacerbate coal-power conflicts during the summer peak. Li stated that safe and stable coal supply is a vital link in energy security. As of June 16, coal inventories at centrally dispatched power plants reached 210 million tonnes, sufficient for an average of 34 days of usage, Li added.

Shaanxi province issued a notice on ensuring energy supply during the 2026 summer peak, explicitly requiring authorities in coal-producing cities to fulfill territorial responsibilities by urging coal enterprises to release advanced capacity in a lawful manner under the precondition of safety, striving for stable output. The province would also strengthen supervision over medium- and long-term contract fulfillment, targeting a monthly fulfillment rate of no less than 90% during the summer peak. Local dispatched power plants are required to raise coal inventories to cover over 20 days of consumption ahead of the summer peak and dynamically eliminate instances where inventory coverage falls below 15 days during the peak period.

Each month, Sxcoal's analyst team conducts a comprehensive analysis of China's thermal coal market from the perspectives of supply/demand, import/export, stock, and price trends. The monthly report also includes insights on the latest coal policies, key events, and forecasts for thermal coal prices for the upcoming month and the remainder of the year.

Prior to the end of each month, Sxcoal publishes the China Thermal Coal Market Monthly Analysis and Forecast.

Sumber:

Artikel Lainnya

Liputan 6

Tayang pada

1,76 Juta Metrik Ton Batu Bara Disebar ke 4 PLTU Jaga Listrik di Jawa Tak Padam

Bisnis Indonesia

Tayang pada

10 dari 190 Izin Tambang yang Dibekukan Sudah Bayar Jaminan Reklamasi

IDX Channel.com

Tayang pada

10 Emiten Batu Bara Paling Cuan di 2024, Siapa Saja?

METRO

Tayang pada

10 Negara Pengguna Bahan Bakar Fosil Terbesar di Dunia

CNBC Indonesia

Tayang pada