SXCOAL

Tayang pada

Monthly: China Jun coastal coal freight rates see pullbacks amid mounting bearish factors

China's coastal coal freight rates trended lower with volatility throughout June, seeing a steep slump late in the month. Weak coal burns and elevated inventories at power plants during the rainy season, together with surging imported cargo inflows and weakening support from seaborne freight markets, significantly weighed on rates.

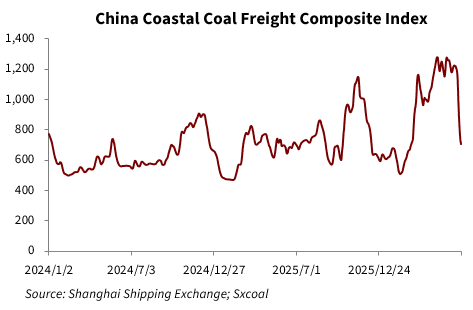

The China Coastal Coal Freight Composite index plunged 43.77% compared to the end of May to 708 as of June 26, representing a year-on-year drop of 1.52%.

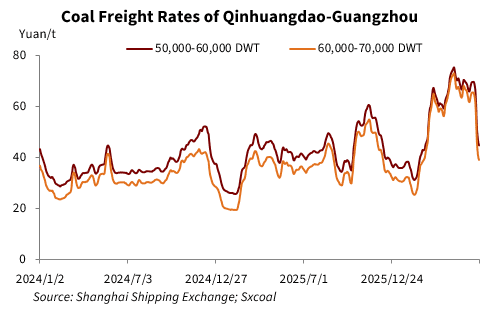

Freight rates on most routes from Qinhuangdao port retreated notably in June. The 40,000-50,000 DWT vessels from Qinhuangdao to Zhangjiagang port plummeted 52% on the month, while the 40,000-50,000 DWT Qinhuangdao to Shanghai vessels plunged 52%.

On June 26, the freight rate for 60,000-70,000 DWT coal vessels on the Qinhuangdao-Guangzhou port route stood at 39.2 yuan/t, diving 27.2 yuan/t or 41% compared to month-ago levels. The rate for the 15,000-20,000 DWT vessels on the Qinhuangdao-Ningbo port route fell 16.4 yuan/t or 27.4% on the month to 43.4 yuan/t.

China's portside thermal coal prices remained firm early last month, while end users largely focused on fulfilling long-term contracts, leaving spot transactions subdued. Meanwhile, the stronger international shipping market attracted more shipowners to overseas routes, lending temporary support to freight rates.

However, as market sentiment cooled at northern ports and traders' bidding prices for utility tenders softened, some utilities shifted to more cost-effective imported cargoes. This weakened support for domestic shipments, particularly on routes to southern China. Ample vessel availability weighed on freight rates.

As the summer peak power season approaches later, power plants have accelerated fulfillment of long-term contracts and increased vessel bookings, providing floor support to freight rates.

Meanwhile, although Chinese utilities remained largely reluctant to accept high-priced spot cargoes, concerns over tight supply and weak import replenishment prompted some low-stock utilities to issue additional spot tenders. Multiple supportive factors lifted vessel demand and fueled freight rate rebounds.

Nevertheless, the growth duration remained limited. As the middle and lower reaches of the Yangtze River entered the rainy season, strong rainfall boosted hydropower output and curbed residential cooling demand, limiting upside potential for coal consumption at coastal power plants. Major utilities held ample stockpiles with comfortable inventory cover days, resulting in weak buying interest and quiet market trading.

Easing geopolitical tensions in the Middle East and the resumption of normal passage through the Strait of Hormuz reduced concerns over risk premiums. At the same time, weakening operational cost support further widened downside pressure on freight rates.

Bearish pressures intensified late in June. Persistent rainfall weighed on residential and industrial power consumption, keeping demand subdued. Weak coal burn at coastal power plants led to slight inventory build-ups due to long-term contract deliveries and imported cargo inflows.

Against this backdrop, end-user procurement cooled amid sluggish demand, resulting in sparse spot transactions. Vessel owners continued to lower freight offers, with rates declining to a three-month low.

The number of anchored vessels hit 157 at peak in the first half of the month, before seeing a pullback in the second half. In the month, averagely 125 vessels anchored at northern ports, down 31 from the previous month, while the average expected arrivals stood at 32, down 1 vessel on the month. As of June 26, there were 62 anchored vessels, down 59 from late May and 25 vessels from the same period last year.

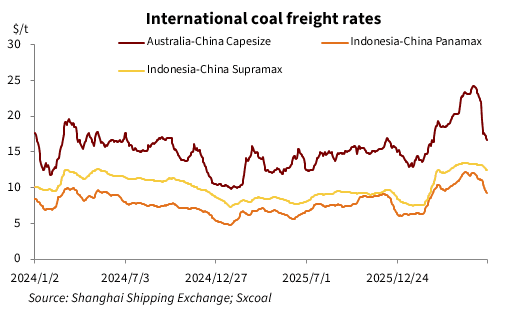

On the international front, the Baltic Dry Index (BDI) also posted a steep retreat across June. On one hand, a large number of newly delivered dry bulk vessels flooded the market in the first half of the year. Coupled with idle capacity released upon the expiry of long-term contracts, empty vessels piled up at major loading ports. Shipowners ramped up freight bidding to secure cargoes, dragging spot freight rates lower. On the other hand, cooling demand for iron ore and metallurgical coal sent Capesize rates tumbling, triggering a downturn across international dry bulk freight markets. As of June 26, the BDI stood at 2,524 points, diving 700 points or 21.71% from late May.

Coal freight rates tracked the downward pullback in the BDI. Separately, easing geopolitical tensions across the Middle East weighed on global coal trading and pressured rates lower. At the same time, major coal importers grew hesitant to take cargoes, slowing logistics turnover and deepening freight declines.

As of June 26, the freight rate for 85,000 DWT vessels from Hay Point, Australia, to Zhoushan, stayed at $18.08/t, down 17.59% or $3.86/t compared to late May. Similarly, for 70,000 DWT vessels from Samarinda, Indonesia, to Guangzhou, the freight rate stood at $9.19/t, decreasing 23.73% or $2.86/t from the end of May.

Looking ahead, end users are expected to prioritize consuming in-plant inventories amid the ongoing rainy season across southern China, sticking to need-based procurement and optimizing calorific value inventory mixes. Freight rates will likely face additional downside pressure on the back of weak vessel booking activity.

Sumber:

Artikel Lainnya

Liputan 6

Tayang pada

1,76 Juta Metrik Ton Batu Bara Disebar ke 4 PLTU Jaga Listrik di Jawa Tak Padam

Bisnis Indonesia

Tayang pada

10 dari 190 Izin Tambang yang Dibekukan Sudah Bayar Jaminan Reklamasi

IDX Channel.com

Tayang pada

10 Emiten Batu Bara Paling Cuan di 2024, Siapa Saja?

METRO

Tayang pada

10 Negara Pengguna Bahan Bakar Fosil Terbesar di Dunia

CNBC Indonesia

Tayang pada