SXCOAL

Tayang pada

Monthly: China Apr thermal coal prices defy seasonal trend amid multi-factor support

China's domestic thermal coal prices rose through April, bucking the typical off-peak trend. Despite the seasonal demand weakness, strong consumption from non-power sectors such as coal chemicals, better-than-expected coal burn in South China, and limited support from imports underpinned the market. Traders showed strong resistance to selling at lower prices, with offers generally trending higher.

March supply-demand summary

Supply China's total thermal coal supply reached 380.22 million tonnes in March, rising 24.01% month on month. Cumulative supply in January-March stood at 1.04 billion tonnes, down 0.07% year on year.

Demand Thermal coal consumption totaled 366.48 million tonnes in March, up 13.39% from a month earlier. Demand over January-March reached 1.08 billion tonnes, increasing 3.33% on the year.

Overall, the market recorded a supply surplus of 13.74 million tonnes in March compared with a shortage of 16.61 million tonnes in the previous month.

Production areas

Coal mines largely maintained normal production and sales in April, with supply staying at relatively high levels. Aside from a few mines undergoing maintenance or face changes, most operations remained stable, with capacity utilization at relatively high levels.

Sxcoal monitoring data showed that, as of April 22, average weekly output stood at 16.96 million tonnes, up 3.6% month on month and 3.2% year on year.

Although demand entered the traditional shoulder season, strong profitability in coal chemical sectors, partly supported by geopolitical tensions, kept operating rates elevated, especially as spring maintenance at some methanol plants was delayed.

This provided solid support to mine-mouth coal demand, with prices generally firm but showing fluctuations in the month.

In terms of inventories, rigid demand from chemical users continued, but weakening third-party coal purchase prices from large coal groups led to a more cautious market tone. Traders at coal yards and railway stations slowed procurement, causing stockpiles at some mines to edge up.

However, with the May Day holiday approaching, pre-holiday restocking demand and improving market expectations are likely to draw down inventories toward the month-end.

As of April 22, stocks at Sxcoal-surveyed mines stood at 4.12 million tonnes, down 2.4% from a month earlier and 6.3% lower year on year.

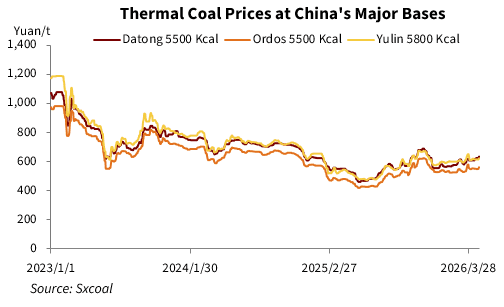

As of April 30, Shanxi Datong 5,500 Kcal/kg NAR thermal coal was assessed at 640 yuan/t, mine-mouth with VAT, rising 20 yuan/t from a month earlier. Inner Mongolia Ordos 5,500 Kcal/kg NAR coal was at 565 yuan/t, dipping 12 yuan/t from the month before, and Shaanxi Yulin 5,800 Kcal/kg NAR thermal coal was assessed at 626 yuan/t, falling 23 yuan/t month on month.

Transfer ports

Coal inventories at northern transfer ports declined notably in April. On the inbound side, although mine shipments remained stable, the Daqin railway entered its annual spring maintenance, cutting daily transport capacity from around 1.2 million tonnes in March to about 1.0 million tonnes.

At the same time, strong chemical demand diverted some cargoes, while negative shipment margins limited incremental flows to northern ports.

High imported coal prices reduced their competitiveness, prompting some demand to shift back to domestic coal. Coastal power plants maintained relatively high burn rates, while some ports accelerated cargo clearance. As a result, outbound shipments remained strong.

Overall, despite stable inflows, stronger outflows led to continued inventory drawdowns at northern ports. However, with stocks falling to moderate levels and congestion easing, the pace of destocking may slow going forward. Traders remained firm in their pricing stance.

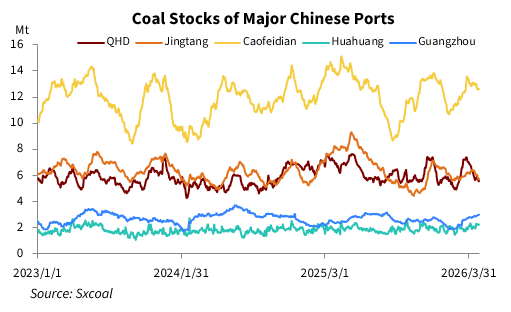

As of April 29, total inventories at major northern ports stood at 26.82 million tonnes, down 6.64% month on month and 13.69% year on year. Qinhuangdao port stocks fell to 5.55 million tonnes, declining 20.71% from a month earlier.

In South China, stronger-than-expected power demand and policy requirements to maintain coal stock supported procurement. As of April 28, Guangzhou port inventories rose to nearly 3 million tonnes, up 7.77% month on month and 21.49% year on year.

As a result, supported by railway maintenance, resilient southern demand, and firm trader sentiment, spot prices continued to rise at northern China ports.

As of April 29, 5,500 Kcal/kg NAR thermal coal traded at Qinhuangdao port reached 800 yuan/t, FOB with VAT, rising 37 yuan/t from the month before.

At southern China's Guangzhou port, Shanxi premium mixed 5,500 Kcal/kg NAR coal with 0.6% sulfur gained 30 yuan/t month on month to 875 yuan/t, ex-stock with VAT. With imported coal remaining uncompetitive in prices, some downstream users increased purchases of domestic coal. This, together with rising offers at northern transfer ports, raised prices of domestic coal prices in South China.

Import market

Imported coal prices remained elevated in April due to tight overseas supply, geopolitical tensions, and rising seaborne freight rates. High landed costs made importers more cautious in bidding, with offer prices edging higher, while domestic demand remained limited to sporadic restocking.

Looking ahead, as temperatures rise and power demand increases, restocking demand for the summer peak season is expected to gradually emerge, with most importers maintaining a relatively optimistic outlook.

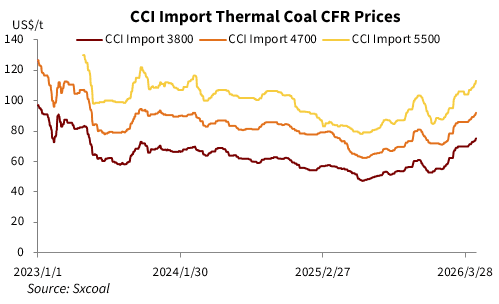

As of April 29, the CCI index for imported 5,500 Kcal/kg, 4,700 Kcal/kg, and 3,800 Kcal/kg NAR coal stood at $114/t, $92.5/t, and $75.5/t CFR, respectively, rising $4.7/t, $2.9/t, and $2.2/t from a month ago.

Consuming areas

Coal consumption at power plants eased slightly in April but remained relatively high compared with historical levels. High imported coal costs limited supplement volumes, while elevated oil prices pushed shipping costs higher, dampening utilities' willingness to dispatch vessels northward.

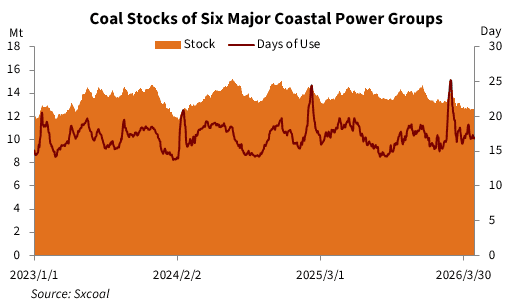

As a result, coal inventories declined at coastal power plants. As of April 29, stocks at power plants under six major coastal power groups stood at 12.64 million tonnes, down 1.65% from end-March and 8.52% lower year on year. Daily consumption was 746,000 tonnes, down 2.23% month on month and 1.97% year on year. Days of inventory stood at 16.9 days, slightly higher month on month but lower than a year earlier.

April highlights recap

The Daqin railway underwent its annual spring maintenance in April, originally scheduled for 30 days but ending three days earlier. While the maintenance reduced transport volumes and led to visible inventory drawdowns at Bohai ports, overall stock levels remained relatively high. However, declining inventories exposed structural tightness in certain coal grades, resulting in vessel queues and supporting market sentiment.

During the month, most listed coal companies released their 2025 annual results and 2026 first-quarter earnings. While 2025 performance generally declined year on year, with some companies slipping into losses, improving coal prices this year have led to a recovery in profitability. Some firms returned to profit on a quarterly basis, for example, Guizhou Panjiang Refined Coal Co., Ltd reported a 143.34% year-on-year increase in Q1 net profit, turning losses into gains.

Meanwhile, several provinces released outlines for their 15th Five-Year Plans, emphasizing energy security and supply stability. Key coal-producing regions reiterated plans to optimize capacity structure, ensure stable output, and maintain adequate production reserves, reinforcing expectations of continued supply resilience.

Each month, Sxcoal's analyst team conducts a comprehensive analysis of China's thermal coal market from the perspectives of supply/demand, import/export, stock, and price trends. The monthly report also includes insights on the latest coal policies, key events, and forecasts for thermal coal prices for the upcoming month and the remainder of the year.

Prior to the end of each month, Sxcoal publishes the China Thermal Coal Market Monthly Analysis and Forecast.

Sumber:

Artikel Lainnya

Liputan 6

Tayang pada

1,76 Juta Metrik Ton Batu Bara Disebar ke 4 PLTU Jaga Listrik di Jawa Tak Padam

Bisnis Indonesia

Tayang pada

10 dari 190 Izin Tambang yang Dibekukan Sudah Bayar Jaminan Reklamasi

IDX Channel.com

Tayang pada

10 Emiten Batu Bara Paling Cuan di 2024, Siapa Saja?

METRO

Tayang pada

10 Negara Pengguna Bahan Bakar Fosil Terbesar di Dunia

CNBC Indonesia

Tayang pada