SXCOAL

Tayang pada

China N port thermal coal grinds toward psychological floor as inventories swell

China's thermal coal prices at northern transshipment ports kept falling toward round-number support levels as the week drew to a close, with bloated inventories at ports and power plants and weak downstream demand leaving sellers little room to defend offers.

Sources reported that offering cargoes around the CCI indices has become increasingly difficult to liquidate, with a discount of 5-10 yuan/t typically required to draw buying interest from end users.

Utilities' buy prices through tenders for 5,000 Kcal/kg NAR coal (S 1%) were heard at 715-719 yuan/t, FOB northern ports with VAT. Blended Ordos same-CV coal (S 0.6%) changed hands around 720 yuan/t for sellers eager to move volume, marking a decline of over 50 yuan/t compared with the recent high in around mid-June.

While some offers of 5,500 Kcal/kg NAR coal hovered in the 800-820 yuan/t range, a deal was reportedly done at a new low of 795 yuan/t, underscoring the widening gap between sell-side expectations and what utilities are willing to pay.

"Some utilities are now holding stockpiles 30-40% above the same period last year, a buffer that has emboldened buyers to push tender prices lower with each round of negotiation," said a trader source in southeastern China.

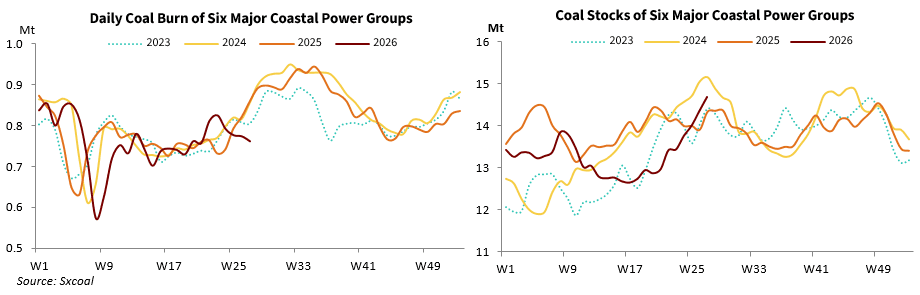

Data showed that coal stocks held by power plants under six major Chinese coastal power groups stood at 14.80 million tonnes on July 2, rising by 3.42% and 11.21% respectively from the week-ago and the month-ago levels, which diverged sharply from downtrends during the comparable 2024 and 2025 periods. The figure exceeded the year-ago level by 3.29%, hitting the highest level since November 16, 2024.

This was partly ascribed to capped heats with ongoing large-scale rainfalls and elevated renewable power generation, which dragged their coal burn well below the seasonal norms.

Port stocks accumulated further, partly due to sluggish power plants' consumption. Sxcoal's data showed on July 3 that total stocks at Qinhuangdao, Caofeidian, Jingtang, and Huanghua ports climbed to 29.40 million tonnes, marking the highest level since late December 2025. Coal outflows from these ports slumped by over 18% from a week earlier.

Production area safety checks have increasingly failed to halt the decline at Bohai ports. Although the overall coal mine capacity utilization in early July remained at a rare low level in Shanxi compared with recent years, based on the latest Sxcoal weekly monitoring data, its impact was increasingly paled at a time when demand presented an anti-seasonal weakness.

Sources broadly agreed that prices have yet to hit the bottom, but also anticipated a slowdown in the decline and restrained downside room. Some participants agreed that 715 yuan/t or so has become the level at which genuine inquiries begin to surface for 5,000 Kcal/kg NAR coal, expecting prices to eventually stabilize around 700-710 yuan/t, a psychological threshold in the coming weeks.

Weather patterns offer a double-edged outlook. While meteorologists forecast a rise in temperatures next week that could boost coal-fired power generation for cooling, the incremental increase in power load is unlikely to materially erode current stockpiles.

"The heat might stabilize prices at best, but it won't drive a rally. By the time August arrives, most end users will have already secured their peak-summer requirements and will only purchase on an as-needed basis," a Beijing-based analyst pointed out.

Besides, recovering LNG-fired power generation following a pullback of the fuel prices also, to some extent, squeezed coal-fired power demand along the eastern coast of China.

Some opportunistic traders have begun accumulating cargoes in anticipation of a potential price bounce in August on the back of late-summer heat, though many seasoned participants view this as a high-risk bet given the entrenched supply surplus.

On July 3, the CCI Index for 5,500 Kcal/kg NAR coal stood at 821 yuan/t FOB with VAT, down 7 yuan/t day on day; the index for 5,000 Kcal/kg NAR and 4,500 Kcal/kg NAR coal also dropped 7 yuan/t to 729 yuan/t and 629 yuan/t, respectively.

Import market drifts lower

The seaborne import segment mirrored the weakness in China's domestic market, with sales pressure persisting and utility tender prices falling further lower amid similarly bloated stocks at southern ports and sluggish power plant consumption.

Bidding prices to a southern Chinese utility for July-delivery Australian 5,500 Kcal/kg NAR coal were heard around 836-848 yuan/t, CFR South China with VAT, implying a Capesize landed cost below $110/t, a level traders described as aggressively low.

The Capesize freight rate from Australia's Newcastle port to South China rebounded slightly to $16/t or so, Sxcoal learned from sources.

The lowest bids for Indonesian 3,800 Kcal/kg NAR coal were heard down to 554 yuan/t or so, CFR with VAT, for August delivery, translating to about $63.1/t FOB on a Panamax basis. The Panamax freight rate also slightly picked up to $8.4-8.6/t from South Kalimantan to South China.

The ongoing weakness was partly impacted by the continued decline in domestic prices, which made imported cargoes uncompetitive again.

Sxcoal's estimate on July 2 showed that Indonesian 3,800 Kcal/kg NAR coal held a price disadvantage of nearly 19 yuan/t compared with its domestic equivalent, shifting from a marginal 5 yuan/t edge in the week prior.

On July 3, the CCI index for Indonesian 3,800 Kcal/kg NAR coal was at $64/t FOB and $74/t CFR, sliding $0.3/t day on day. The index for Australian 5,500 Kcal/kg NAR coal was down $0.5/t at $111/t CFR.

Sumber:

Artikel Lainnya

Liputan 6

Tayang pada

1,76 Juta Metrik Ton Batu Bara Disebar ke 4 PLTU Jaga Listrik di Jawa Tak Padam

Bisnis Indonesia

Tayang pada

10 dari 190 Izin Tambang yang Dibekukan Sudah Bayar Jaminan Reklamasi

IDX Channel.com

Tayang pada

10 Emiten Batu Bara Paling Cuan di 2024, Siapa Saja?

METRO

Tayang pada

10 Negara Pengguna Bahan Bakar Fosil Terbesar di Dunia

CNBC Indonesia

Tayang pada