SXCOAL

Tayang pada

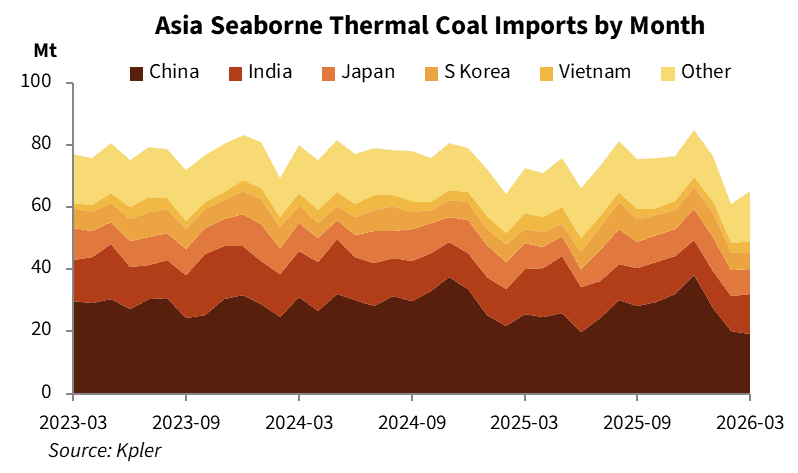

Asia Mar seaborne thermal coal imports split across region; rebound expected

Seaborne thermal coal imports into Asia for March 2026 rebounded from a four-year low in February, but stayed well below year-ago levels as demand diverged sharply across the region. Seaborne coal prices still stayed high, in spite of moderate declines, impacted by supply constraints, logistics among other factors.

Total imports stood at 665.18 million tonnes in March, down 10.26% year on year (YoY) but up 6.79% month on month (MoM), according to vessel-tracking data from Kpler.

China's seaborne thermal coal imports fell 25.58% YoY to 19.10 million tonnes in March, down 5.68% MoM. Domestic coal supply continued to improve, with inventories at Bohai-rim ports building up through March. Coastal domestic coal shipments from north to south reached a nine-month high of 19.90 million tonnes, replacing some seaborne demand, Kpler said.

Even as thermal power generation saw an increase in the second half of March due to weaker wind, solar, and gas-fired output in coastal provinces, utilities held back on overseas purchases amid ample stockpiles.

However, a one-month spring maintenance on Daqin railway starting in April is expected to cut daily rail volumes by more than 10% from March levels, potentially driving a temporary rebound in demand for imported coal.

India brought in 12.87 million tonnes of seaborne thermal coal in March, down 11.64% YoY but up 13.72% MoM. Domestic coal production stood near 114 million tonnes in the month, slightly below the year-ago level, while power demand has been weaker than last year since February, capping immediate growth in coal-fired generation.

Still, Kpler expected the upcoming summer heat to drive a substantial demand pickup. With a low base last year and forecasts for above-normal temperatures, India's thermal coal imports are likely to resume YoY growth in the coming months.

Petroleum coke prices eased after the U.S.-Iran ceasefire announcement, but India's cement sector remains primarily coal-fired, providing baseline support for thermal coal demand.

Japan imported 8.13 million tonnes in March, down 2.9% YoY and 0.64% MoM. South Korea imported 5.03 million tonnes, up 17.86% YoY but down 16.13% MoM.

Although about 10.4 GW of nuclear capacity will come online in Japan during April-May, that will mainly displace gas rather than coal, leaving the thermal coal consumption outlook firm, Kpler noted. At current price levels, Indonesian high-quality coal is the most competitive source for the Japanese market.

South Korea's nuclear available capacity is expected to drop 3 GW YoY, while the retirement of some old coal units has been delayed, meaning coal power remains critical in the second and third quarters.

In Southeast Asia, Vietnam was the largest seaborne thermal coal importer with 4.13 million tonnes, down 22.8% YoY but up 42.84% MoM. Kpler anticipated Vietnamese coal demand to recover gradually in the coming months as the dry season approaches and the country moves to bolster coal supply security. Potential El Nino-related temperature rises could further lift power and coal demand.

The Philippines imported 2.99 million tonnes, up 4.25% YoY and 10.21% MoM. Reduced LNG supply reduced gas-fired power availability, a trend likely to deepen the country's power-sector reliance on coal.

The temporary U.S.-Iran peace deal lowered the risk of escalation, but the risk of a Strait of Hormuz blockade persists, threatening LNG and petroleum coke supply and potentially boosting coal demand, Kpler said.

Seaborne thermal coal prices are projected to face downward pressure as gas prices will retreat during the ceasefire period, but underlying support remains. No LNG tankers have yet headed toward the Strait since the truce.

Kpler's latest price forecast cut its second-quarter 2026 ARA price to $113/t CIF from $128/t, and Newcastle price to $128/t FOB from $135/t. Smaller adjustments for the third quarter and beyond reflect market expectations of continued uncertainty.

The Asian thermal coal market is in a transitional phase under short-term pressure but with medium-term support. China may see higher April imports due to domestic logistics tightening, while India's approaching summer heat wave will drive procurement.

On the supply side, Indonesia is pivoting toward higher output, though full-year production may still fall YoY. Australia's long-term exports face policy constraints, and Russia benefits from a geopolitical premium but faces rising security risks.

While the ceasefire has created short-term price downside, actual shipping through the Strait of Hormuz has not resumed, and participants are generally building inventories against uncertainty. That means thermal coal prices, after phased adjustment, will continue to find solid support from both demand and costs in the coming months.

Sumber:

Artikel Lainnya

Liputan 6

Tayang pada

1,76 Juta Metrik Ton Batu Bara Disebar ke 4 PLTU Jaga Listrik di Jawa Tak Padam

Bisnis Indonesia

Tayang pada

10 dari 190 Izin Tambang yang Dibekukan Sudah Bayar Jaminan Reklamasi

IDX Channel.com

Tayang pada

10 Emiten Batu Bara Paling Cuan di 2024, Siapa Saja?

METRO

Tayang pada

10 Negara Pengguna Bahan Bakar Fosil Terbesar di Dunia

CNBC Indonesia

Tayang pada